How Compound Interest Works

Albert Einstein may or may not have called compound interest the eighth wonder of the world. The quote is probably made up. But the sentiment is correct, and understanding how compounding works is probably the single most useful thing you can do before you invest a penny.

The concept is simple. The numbers, over long enough periods, are staggering.

The Basic Idea

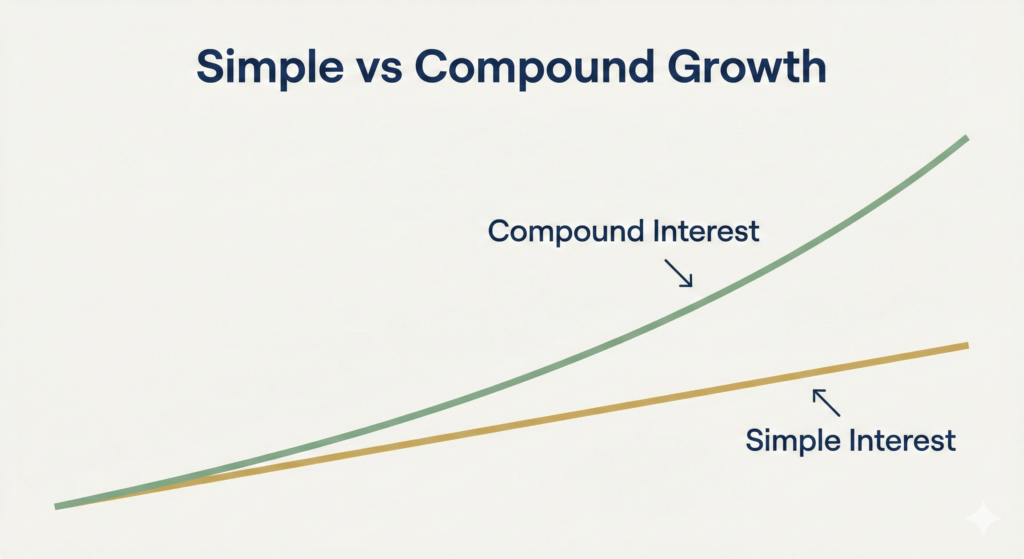

With simple interest, you earn a return only on the original amount you invested, your principal. With compound interest, you earn a return on your principal AND on all the returns you’ve already made.

Your returns start earning returns. And those returns earn returns. Over time, this creates a snowball effect that gets faster and faster.

| Simple vs compound, a side-by-side You invest £10,000 at a 7% annual return. With simple interest: you earn £700 every year. After 20 years, you have £24,000. With compound interest: in year one you earn £700. In year two you earn 7% on £10,700, which is £749. In year three you earn 7% on £11,449, which is £801. And so on. After 20 years, you have £38,697. Same starting amount. Same return. A difference of over £14,000, just from letting the returns compound. |

Why Time Is the Critical Ingredient

Compounding grows slowly at first and then dramatically fast. In the early years it barely feels like anything is happening. In the later years it becomes almost hard to believe.

This is why the length of time you’re invested matters far more than the amount you start with. A smaller amount invested earlier will almost always beat a larger amount invested later.

| Sarah and James, a tale of two investors Sarah starts investing £200 a month at age 25. She invests for 10 years then stops completely and never adds another penny. By age 65, assuming 7% annual growth, she has approximately £263,000. James waits until he’s 35 then invests £200 a month for 30 years straight, three times as long as Sarah and three times as much total money invested. By age 65, James has approximately £243,000. Sarah put in £24,000. James put in £72,000. Sarah has more. The only difference is that Sarah started 10 years earlier and let compounding do its work. |

This example isn’t designed to make you feel guilty if you haven’t started yet. It’s designed to show you that starting now, even with a modest amount, is genuinely worth it. The second best time to start is always today.

How Investment Returns Compound

In investing, compounding happens through two mechanisms: the growth in the value of your investments, and any dividends or income they pay out.

Most index funds automatically reinvest dividends, so rather than paying out the income to you in cash, they buy you more units of the fund. Those extra units then grow along with everything else. This is called dividend reinvestment, and over decades it can account for a significant portion of your total return.

This is why it’s important, when you’re looking at investment performance, to check whether a figure includes reinvested dividends or not. Many headline figures don’t, and they significantly understate what a real long-term investor would have actually made.

The Impact of Fees on Compounding

Compounding works in both directions. Just as your returns compound upward over time, so do fees compound against you.

A fund charging 1.5% per year in fees versus one charging 0.15% per year sounds like a tiny difference. Over 30 years, on a £50,000 investment, that difference costs you over £100,000 in lost returns. The fee is compounding against you every single year, eating into money that should have been growing.

This is why low-cost index funds are so central to sensible long-term investing. We cover this in much more detail in our page on why fees destroy your returns.

| The rule of 72 A useful mental shortcut: divide 72 by your annual return rate to find roughly how many years it takes to double your money. At 7% annual growth, your money doubles approximately every 10 years. At 4%, every 18 years. At 2% (a typical savings account rate), every 36 years. That’s the difference between investing and just saving. |

What Rate of Return Should You Expect?

Compounding examples tend to use round numbers like 7% or 8%. Where do those figures come from, and are they realistic?

They’re based on long-run historical stock market returns. The US stock market has returned around 10% per year on average over the last century. Adjusted for inflation, that’s closer to 7%. Global markets have been slightly lower. Past performance is not a guarantee of future results, that’s a legal requirement to say, and also genuinely true.

What we can say is that over long enough periods, diversified investing in the global stock market has consistently outperformed cash and inflation. There’s no certainty in investing. But the long-term direction of travel has been upward.

| Important: short-term volatility is real Compounding works over the long term, but markets don’t go up in a straight line. There will be years where your portfolio drops 20%, 30%, or more. The people who benefit from compounding are the ones who don’t panic and sell at those moments. Time in the market matters far more than timing the market. |

How to Make Compounding Work For You

The practical implications of compound interest are straightforward:

- Start as early as you can, even if the amounts feel small

- Invest consistently, regular contributions beat trying to time the market

- Reinvest any dividends rather than taking them as cash

- Keep fees as low as possible, every percentage point compounds against you

- Leave your investments alone, selling during market falls breaks the compounding cycle

| Not financial advice This page explains how compound interest works as a mathematical concept. It is not a prediction of future returns or a recommendation of any specific investment. Always invest in line with your own circumstances and risk tolerance. |

What Next?

Now that you understand what compounding does, the natural next question is: how much does it cost me to wait? Our page on the cost of waiting puts real numbers on it. Or if you’re ready to get started, your first steps explains what to actually do.