Inheritance Tax Basics

Most estates pay no inheritance tax at all. Here is how the rules work and what actually triggers a bill.

This page covers general information about inheritance tax rules as they currently stand. Tax rules and legislation change. The proposed changes to pension inheritance tax treatment from April 2027 are not yet finalised. This is not financial or legal advice. Consult a qualified financial adviser or solicitor for guidance specific to your situation.

The basics

Inheritance tax (IHT) is charged on the value of your estate, which is your assets minus your debts, above certain thresholds. The rate is 40% on anything above the threshold. It is paid by your estate before anything is distributed to your beneficiaries.

The first thing to understand is that most estates pay no IHT at all. HMRC figures consistently show that only around 4% of deaths result in an IHT bill. The thresholds are high enough that the majority of people are not affected.

For people accumulating significant assets over a long investment horizon, which describes anyone seriously pursuing financial independence, it is worth understanding how the rules work and how different types of asset are treated.

The Thresholds

The nil rate band

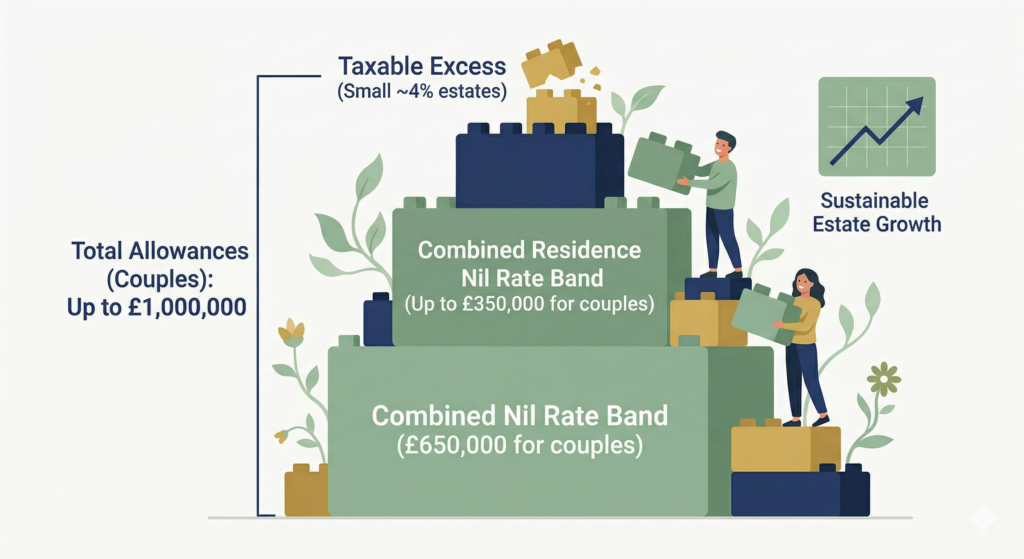

Every individual has a nil rate band of £325,000. Assets up to this value pass free of IHT. Anything above it is taxed at 40%.

If you are married or in a civil partnership, any unused nil rate band can be transferred to your surviving spouse on your death. This means a married couple can effectively combine their allowances, passing up to £650,000 free of IHT.

The residence nil rate band

An additional allowance applies if you own a property and leave it to direct descendants, meaning children or grandchildren. This residence nil rate band is currently £175,000 per person, or up to £350,000 for a couple.

Combined with the standard nil rate band, a married couple leaving their main home to their children can pass up to £1,000,000 free of IHT.

The residence nil rate band tapers for estates above £2,000,000. It reduces by £1 for every £2 above that threshold, disappearing entirely for very large estates.

How Different Assets Are Treated

Not all assets are treated the same way for IHT purposes. This is one of the most important things to understand if you are building a diversified portfolio.

ISAs

ISAs form part of your estate. A Stocks and Shares ISA worth £200,000 at death adds £200,000 to your taxable estate. The ISA wrapper provides income tax and capital gains tax advantages during your lifetime, but it confers no IHT advantage on death.

General Investment Account

A GIA forms part of your estate at full market value on death. There is no special treatment.

Main residence

Your home forms part of your estate. It may be eligible for the residence nil rate band if left to direct descendants, as described above.

Pensions

Pensions currently sit outside your estate entirely. A SIPP worth £500,000 is not counted in your taxable estate. This has historically made pensions an extremely efficient vehicle for passing wealth to the next generation, since you can draw from ISAs and other assets first in retirement while leaving the pension untouched to pass on free of IHT.

However, the government announced in the 2024 Autumn Budget that pensions will be brought within the scope of IHT from April 2027. This is a significant proposed change that would fundamentally alter how pensions are treated in estate planning. The rules are not yet finalised and are subject to ongoing consultation. Check the current position before making any decisions based on this.

Business assets and AIM shares

Certain business assets may qualify for Business Relief, which can reduce or eliminate IHT on qualifying assets. This is specialist territory and worth discussing with a financial adviser if it is relevant to your situation.

Gifts and the Seven Year Rule

Gifts made during your lifetime are not automatically exempt from IHT. The rules work as follows.

Potentially exempt transfers

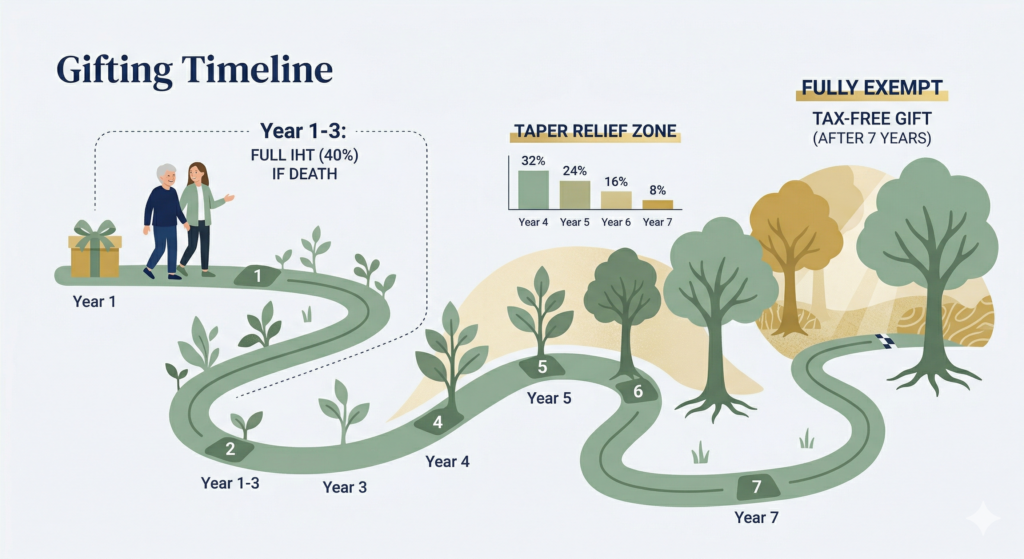

If you give money or assets to another individual, the gift becomes fully exempt from IHT if you survive for seven years after making it. If you die within seven years, the gift may be subject to IHT on a sliding scale known as taper relief. The full 40% rate applies if you die within three years. The rate reduces gradually between three and seven years.

Annual exemption

You can give away up to £3,000 per tax year free of IHT, regardless of the seven year rule. Any unused annual exemption can be carried forward by one year.

Small gifts

You can give up to £250 per person per tax year to any number of people free of IHT. This cannot be combined with the annual exemption for the same recipient.

Wedding and civil partnership gifts

You can give up to £5,000 to a child, £2,500 to a grandchild, and £1,000 to anyone else, free of IHT, as a gift on the occasion of a marriage or civil partnership.

Regular gifts from income

Gifts that form part of a regular pattern and are made from surplus income rather than capital can be exempt from IHT regardless of the seven year rule. This is a useful exemption for people with income they do not need to spend, but it requires clear documentation to demonstrate the pattern and the surplus income. Speak to a financial adviser if you want to use this exemption.

Other Exemptions

The spousal exemption

Assets passing between spouses or civil partners are entirely exempt from IHT, regardless of value. You can leave everything to your spouse with no IHT consequence. This simply defers the question to when the surviving spouse dies, at which point the combined estate is assessed.

Charitable gifts

Gifts to registered charities are exempt from IHT. If you leave at least 10% of your net estate to charity, the IHT rate on the remainder reduces from 40% to 36%.

Is IHT Relevant to You?

A quick sense check:

Add up your assets, including property, savings, ISAs, GIA, any life insurance not written in trust, and other assets. Subtract any debts, including your mortgage. If the result is below £325,000 for a single person or £650,000 for a married couple, IHT is unlikely to be an issue at current thresholds.

If you own a home and are married, and plan to leave it to your children, the combined threshold rises to £1,000,000 as described above.

If you are on a long FIRE journey and accumulating assets over decades, the picture can change. A portfolio that looks comfortably below the threshold today may look different in twenty years, particularly if property values have risen alongside investment growth. It is worth revisiting the question periodically rather than assuming IHT will never apply to you.

What to do if IHT is relevant

The starting point is not IHT planning. It is making sure the foundations are in place first: a current will, a registered power of attorney, and up to date pension nominations. IHT planning built on that foundation makes sense. IHT planning without those basics in place does not.

If your estate looks likely to exceed the thresholds, a financial adviser or specialist estate planner can help you think through the legitimate options available, including gifting strategies, trusts, pension planning, and life insurance written in trust to cover the eventual bill. These are all legal and well established approaches, but they interact with your overall financial plan in ways that need proper consideration.

See the wills and LPA guide and the pension beneficiaries guide if you have not worked through those yet.

What’s Next

You have now covered all four areas of protecting your wealth. If you have not yet worked through the earlier guides in this section, the natural starting point is making sure your will and power of attorney are in order before thinking about anything else.

This is general information about inheritance tax rules as they currently stand. Tax rules change. The proposed pension IHT changes from April 2027 are not yet finalised. This is not financial or legal advice. Consult a qualified financial adviser or solicitor for guidance specific to your situation.