Lifetime ISA (LISA): Who It’s For and How It Works

The Lifetime ISA is one of the most generous government benefits available to younger UK investors, a free 25% top-up on everything you put in. It’s also one of the most misunderstood accounts, with a withdrawal penalty that catches people out badly if they use the money for the wrong purpose.

This guide covers what the LISA offers, who it’s designed for, and, crucially, when you should and shouldn’t use one.

| Key Facts at a Glance Who can open one: UK residents aged 18-39 Annual contribution limit: £4,000 per tax year Government bonus: 25% of contributions, up to £1,000 per year Counts toward ISA allowance: Yes, the £4,000 is part of your £20,000 annual ISA allowance Valid uses: Buying your first home (under £450,000) or retirement from age 60 Withdrawal penalty: 25% of the withdrawal amount, effectively losing your bonus plus some of your own money Account types: Stocks and Shares LISA or Cash LISA |

The 25% Government Bonus: How It Works

For every pound you put into a Lifetime ISA, the government adds 25 pence. Contribute the maximum £4,000 in a tax year and you receive a £1,000 bonus, giving you £5,000 invested. The bonus is paid monthly by HMRC directly into your LISA account.

| The bonus in practice You open a Lifetime ISA at 25 and contribute £4,000 per year until you’re 50, the maximum eligible age. Over 25 years you contribute £100,000 of your own money. The government adds £25,000 in bonuses. That £25,000 then grows alongside your contributions for potentially decades. The bonus alone is worth a significant amount by the time you reach 60, and that’s before any investment growth on the bonus itself. |

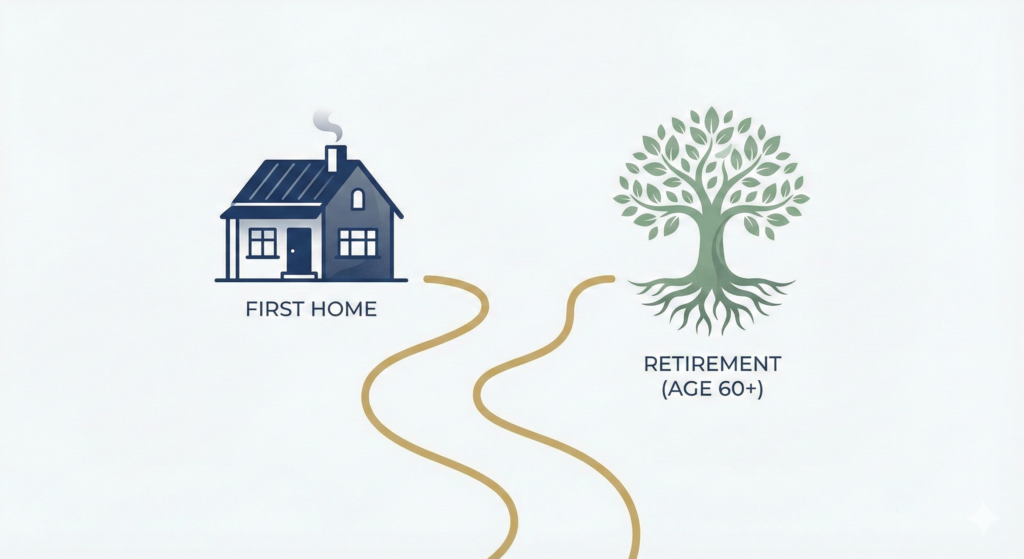

The Two Permitted Uses

Buying your first home

You can use your LISA savings toward the purchase of your first property, provided the property costs £450,000 or less. The money goes directly to your solicitor as part of the conveyancing process, you don’t withdraw it yourself.

You must have had the LISA open for at least 12 months before using it for a property purchase. This makes opening one early, even with a small contribution, a sensible move if buying a home is a future possibility.

Retirement from age 60

From your 60th birthday, you can withdraw all your LISA savings, contributions and bonuses, completely tax-free, for any purpose. There’s no restriction on what you spend the money on.

This makes the LISA a legitimate retirement savings vehicle for younger people, particularly those who are self-employed and don’t have access to an employer pension scheme. The 25% bonus is equivalent to basic-rate tax relief on a pension, making the comparison between the two genuinely competitive for some investors.

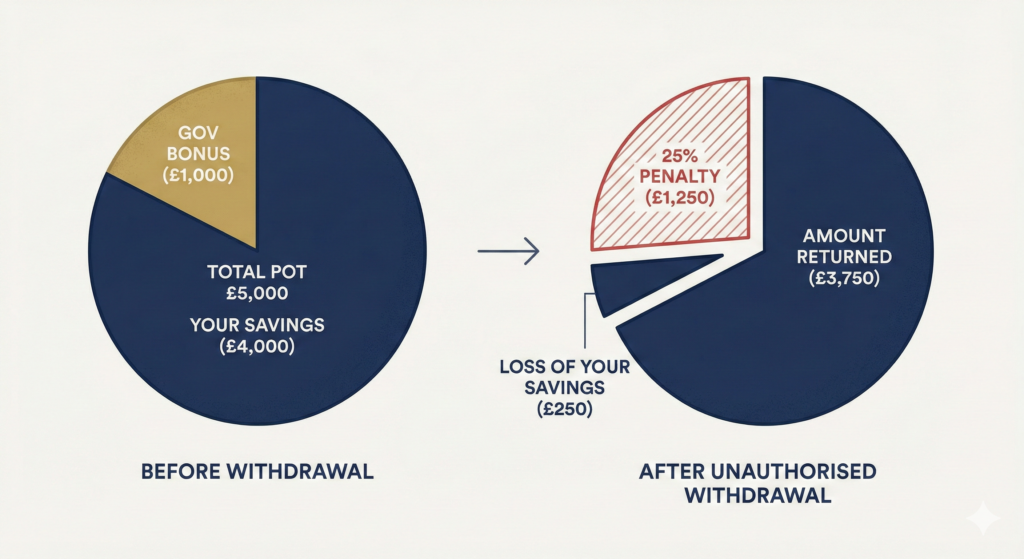

The Withdrawal Penalty: Read This Carefully

If you withdraw money from a Lifetime ISA for any reason other than buying a qualifying first home or retirement after 60, including a financial emergency, a non-qualifying property purchase, or simply changing your mind, you pay a 25% penalty on the withdrawal amount.

| The penalty costs more than your bonus This is the part that surprises people. The penalty is 25% of the withdrawal amount, not 25% of the bonus. Because the bonus has already been added to your pot, the 25% penalty effectively takes back the bonus AND a small slice of your own contributions. Example: You contribute £4,000. With the 25% bonus, your pot is £5,000. You withdraw the full £5,000 as an unauthorised withdrawal. The 25% penalty is £1,250, leaving you with £3,750. You put in £4,000 and got back £3,750. You’ve lost £250 of your own money, not just the bonus. |

This penalty was temporarily reduced to 20% during Covid, but returned to 25% in April 2021. There is no flexibility, terminal illness and age 60 are the only exceptions to the penalty.

LISA vs Pension: Which Should You Use?

This is one of the most common questions about the LISA, and the honest answer is: it depends on your circumstances, but for most employed people a pension comes first.

| Factor | Lifetime ISA | Pension / SIPP |

| Government bonus / tax relief | 25% on contributions | 20% basic rate, 40% higher rate, 45% additional rate |

| Employer contributions | None | Many employers match or top up your contributions, free money |

| Access age | 60 (LISA) | 57 rising to 58 in 2028 (pension) |

| Annual limit | £4,000 | £60,000 (or 100% of earnings if lower) |

| Tax on withdrawal | Tax-free | Tax-free lump sum (25%) then taxed as income |

| Means-tested benefits | Counted as an asset | Not counted until drawdown age in most cases |

| Best for | First-time buyers; self-employed under 40 | Employed workers; higher-rate taxpayers; long-term retirement savings |

For employed workers with access to a workplace pension, especially one with employer matching, the pension almost always wins. The employer contribution is free money that no LISA bonus can match.

For self-employed people under 40 who don’t have access to an employer scheme, the LISA bonus is equivalent to basic-rate pension tax relief, making it genuinely competitive. Many self-employed investors use both, LISA up to the £4,000 limit, then additional savings into a SIPP.

Who the LISA Is and Isn’t Right For

| Profile | Is a LISA Right for You? |

| First-time buyers under 40 | Excellent, the 25% bonus on your deposit savings is substantial and the 12-month rule makes opening early a priority. |

| Self-employed under 40 | Very good, equivalent to basic-rate pension tax relief with the flexibility of an ISA-style structure. |

| Employed workers with a workplace pension | Use sparingly, max your employer match in your pension first. LISA for first home only if applicable. |

| Higher-rate taxpayers | Pension tax relief (40%) beats the LISA bonus (25%) significantly. Pension first. |

| Anyone who might need the money before 60 | Proceed with caution, the penalty structure means accessing LISA funds early is genuinely costly. |

| Over 40s | Cannot open a new LISA. Can contribute to an existing one until 50. |

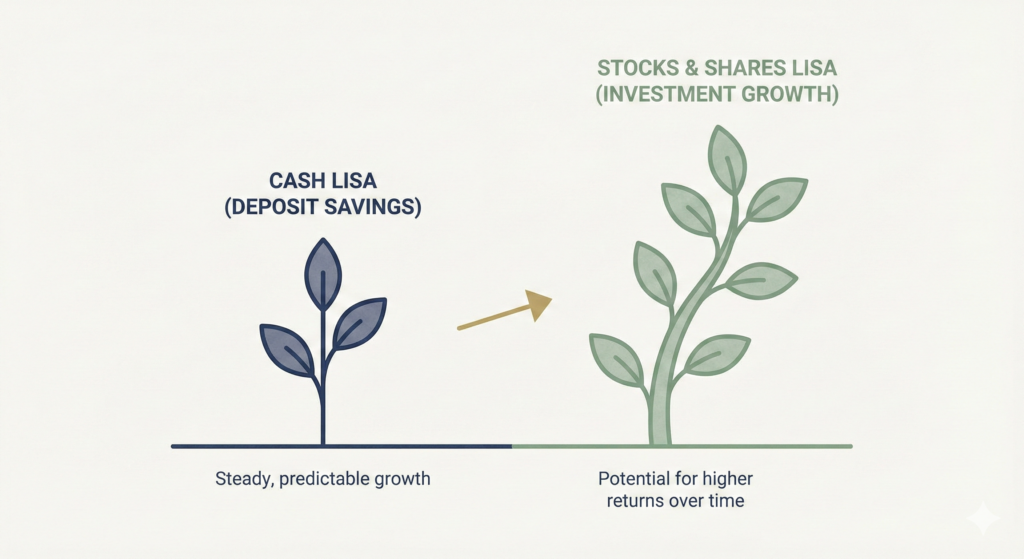

Stocks and Shares LISA vs Cash LISA

A Cash LISA holds your savings in cash, earning interest, similar to a savings account. A Stocks and Shares LISA invests your savings in funds or shares, with the potential for higher returns alongside market risk.

For someone saving for a house purchase in the next 2-3 years, a Cash LISA preserves your deposit. For someone using the LISA primarily for retirement savings with a long time horizon, a Stocks and Shares LISA typically makes more sense, the investment returns over decades can significantly outpace cash interest rates, and the same arguments for investing over saving apply.

| Not financial advice This page explains how Lifetime ISAs work based on current HMRC rules as of the 2024/25 tax year. The rules around the withdrawal penalty, property price caps, and contribution limits are subject to change. Always verify current rules at gov.uk before opening a LISA or making decisions based on them. This is not personalised financial advice. |

What Next?

If you’re employed and saving primarily for retirement, our SIPP and pension guide covers how pension investing works, the tax relief you’re entitled to, and how a Self-Invested Personal Pension compares to a workplace scheme. Or if you’re ready to look at the practical question of which platform to use, our UK platform comparison covers the main options for Stocks and Shares ISAs, LISAs, and SIPPs side by side.