How to Diversify Your Investments

Diversification is one of those investing concepts that sounds technical but is actually intuitive once you understand it. The core idea is simple: don’t put all your eggs in one basket. The application of that idea, done properly, is what separates a robust long-term portfolio from a fragile one.

This page explains what diversification actually means in practice, how a global index fund achieves most of it automatically, and the mistakes people make thinking they’re diversified when they aren’t.

The Basic Principle

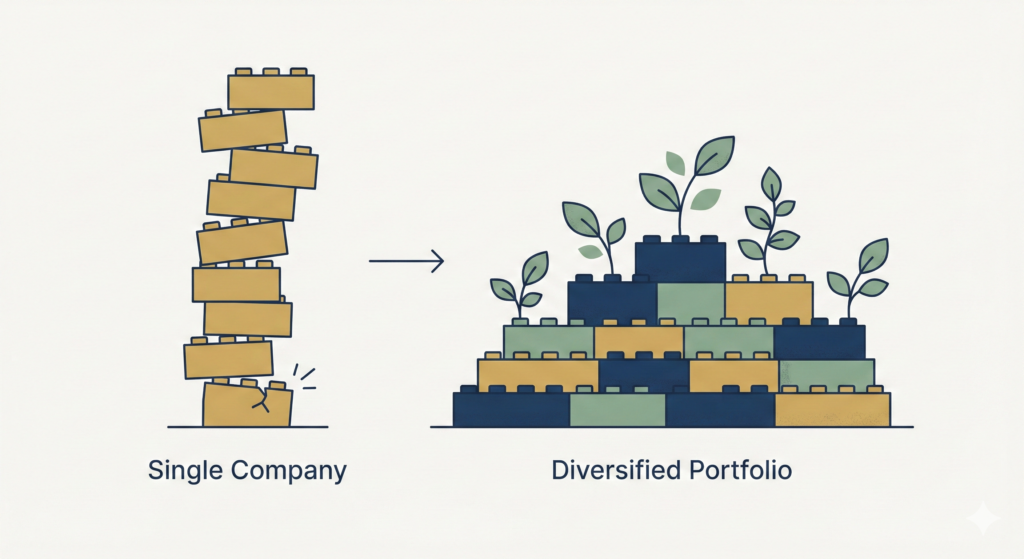

When you invest in a single company’s shares, your outcome is entirely tied to that company. If it thrives, you do well. If it struggles, bad management decision, product failure, regulatory problem, genuine bad luck, your investment takes the full hit. If it fails entirely, you lose everything you put in.

Diversification spreads your money across many different investments so that no single failure can seriously damage your overall position. The more truly independent your holdings are, different companies, different industries, different countries, different asset types, the more protected you are from any one of them going wrong.

| A concrete illustration Investor A puts £10,000 into one UK bank’s shares. Investor B puts £10,000 into a global index fund holding 3,500 companies across 50 countries. The bank has a difficult year, shares fall 40%. Investor A’s £10,000 is now £6,000. The same difficult year for banks affects Investor B’s global fund, but banks are only one sector among dozens, and UK banks are a fraction of a globally diversified portfolio. The fund might fall 5-8% in a bad year for banks. Investor B’s £10,000 is around £9,200. Same market event. Very different outcomes. |

What You’re Actually Diversifying Across

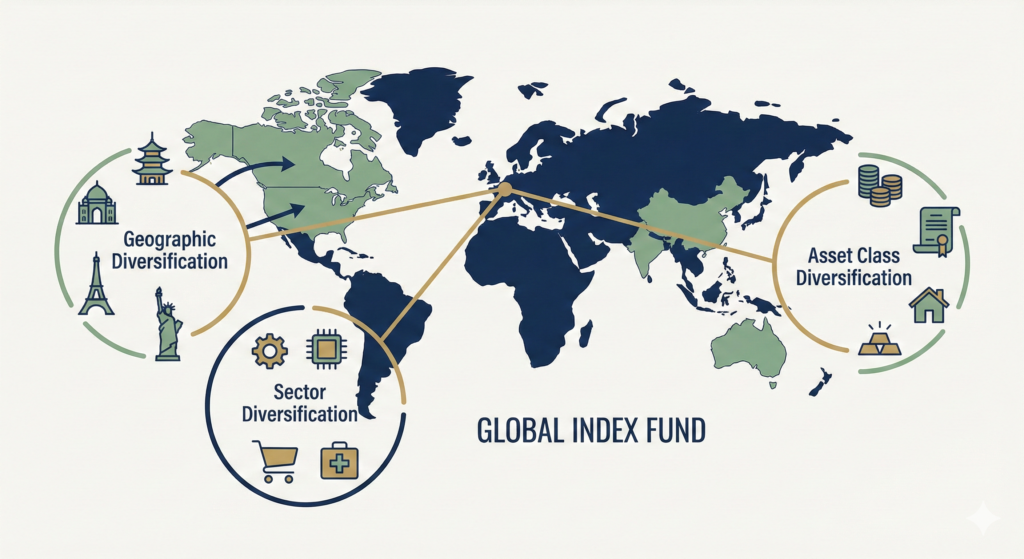

True diversification works on several levels simultaneously. Most people understand company-level diversification, own many companies, not just one. But there are other dimensions that matter just as much.

Geographic diversification

Different countries have different economic cycles, political environments, and growth trajectories. A portfolio concentrated in one country, even a large one, is exposed to country-specific risks: regulatory changes, political instability, currency movements, or an entire economy going through a bad period.

A global fund spreads across the US, UK, Europe, Japan, emerging markets, and more. When one region struggles, others may be doing well. The overall portfolio smooths out.

Sector diversification

Different sectors of the economy behave very differently at different times. Technology companies tend to do well in periods of growth and poorly when interest rates rise sharply. Energy companies often move with oil prices. Consumer staples, food, household goods, tend to be stable even in recessions because people still need to eat and clean their homes.

A portfolio concentrated in one sector is highly exposed to that sector’s specific risks. A global index fund automatically holds technology, financials, healthcare, consumer goods, energy, industrials, and more, in proportion to their market size.

Asset class diversification

Beyond shares (equities), investors can hold bonds, property, commodities, and cash. These different asset classes don’t always move in the same direction, bonds, for example, have historically risen when equities fall, providing a cushion during stock market downturns.

For long-term investors many years from retirement, a portfolio heavily weighted to equities makes sense, the long time horizon absorbs the volatility. As you get closer to needing the money, adding bonds and reducing equity exposure reduces the risk of a major market fall hitting you at exactly the wrong moment.

| Asset Class | Role in a Portfolio |

| Equities (shares) | Ownership in companies. Highest long-term growth potential, highest short-term volatility. Core of most long-term portfolios. |

| Bonds | Loans to governments or companies. Lower return than equities over long periods, but more stable. Good counterbalance to equity risk. |

| Property / REITs | Exposure to property markets through funds (Real Estate Investment Trusts). Provides some inflation protection and income. |

| Cash | Savings accounts, money market funds. Essential for emergency fund and short-term needs. Loses purchasing power to inflation over time. |

| Commodities | Gold, oil, agricultural products. Can provide inflation hedge and portfolio stability. Not essential for most ordinary investors. |

How a Global Index Fund Diversifies You Automatically

This is the practical punchline for most readers on this site: a single global index fund does the heavy lifting of diversification for you.

Take Vanguard’s FTSE All-World ETF as an example. It holds over 3,500 companies across more than 50 countries. It includes large, medium, and smaller companies. It spans every major economic sector. Within a single fund, you have geographic, sector, and company diversification covered.

| What a global index fund gives you Company diversification: 3,500+ companies, no single company is more than ~4% of the fund Geographic diversification: US (~60%), Europe (~15%), Japan (~6%), UK (~4%), emerging markets (~10%), other Sector diversification: technology, financials, healthcare, consumer, industrials, energy, and more Automatic rebalancing: as companies grow or shrink, the fund adjusts without you doing anything |

For many investors, this is genuinely all the diversification they need. One fund. One purchase. Automatically diversified across the global economy.

Common Diversification Mistakes

Diversification sounds simple, but there are several ways investors think they’re diversified when they aren’t. These are worth understanding.

Owning many funds that hold the same things

Buying five different global equity funds doesn’t give you five times the diversification, it gives you roughly the same diversification as one, with more complexity and potentially higher fees. If all five funds track the same index, you own the same companies five times. True diversification comes from owning genuinely different things, not multiple funds that overlap heavily.

Home country bias

UK investors have a tendency to overweight UK shares. This feels comfortable, we understand British companies, we use their products, we follow them in the news. But the UK stock market represents around 4% of global market capitalisation. A portfolio that’s 50% UK shares is massively overexposed to one small corner of the global economy.

| The home bias problem in numbers The UK makes up roughly 4% of the world’s investable stock market. If you hold 40% of your portfolio in UK shares, you’re 10 times more concentrated in the UK than a truly global index. If the UK economy underperforms globally, as it has at various points, your portfolio underperforms too, not because you made bad choices but because of unnecessary concentration. |

Confusing variety with diversification

Owning shares in ten different technology companies is not the same as being diversified. Ten tech companies will largely rise and fall together because they’re all affected by the same forces, interest rate changes, regulation of big tech, the appetite for growth investing. True diversification requires holdings that aren’t tightly correlated, that don’t all move in the same direction at the same time.

Ignoring time diversification

Regular investing, putting money in every month regardless of what markets are doing, is a form of time diversification. Rather than investing a lump sum at one moment in time (and risking that it’s a market peak), you’re spread across different entry points over months and years. This is pound-cost averaging, and it’s a meaningful part of a well-diversified approach.

How Much Diversification Is Enough?

Research suggests that most of the diversification benefit within equities is achieved with around 20-30 carefully chosen uncorrelated stocks. Beyond that, adding more individual stocks adds very little additional protection.

A global index fund gives you thousands of companies and handles all of this automatically. For most investors the question isn’t ‘how do I diversify?’ but ‘what’s the simplest way to achieve good diversification?’, and the answer is a single global index fund.

As your portfolio grows and you get closer to retirement, adding a bond fund to your equities is the main additional diversification step most investors need to consider. A 70/30 or 60/40 split between equities and bonds is a common target for investors approaching retirement age.

| A simple diversified portfolio for most investors For investors with a long time horizon (10+ years): one global equity index fund (e.g. FTSE All-World) For investors closer to needing the money: a global equity index fund plus a global bond index fund, with the bond proportion increasing as you approach your target date This two-fund approach is genuinely all most ordinary investors need. Complexity beyond this rarely adds proportionate benefit. |

What Diversification Can and Cannot Do

Diversification is powerful, but it’s worth being clear about its limits.

What it does: removes the risk that any single company, sector, or country failure will seriously damage your portfolio. It smooths your returns over time and prevents catastrophic losses from concentration.

What it doesn’t do: protect you from overall market falls. In a global recession or financial crisis, a globally diversified equity portfolio will still fall, sometimes significantly. Diversification doesn’t eliminate market risk, it eliminates the additional risk of concentration. The way to reduce market risk is to include other asset classes like bonds, or to hold more cash.

| Diversification and market crashes In severe market downturns, correlations between asset classes often increase, meaning things that usually don’t move together start moving together. In the 2008 financial crisis, almost all equity markets fell simultaneously. Diversification within equities helped, but the best protection was holding bonds and cash alongside equities. This is why asset class diversification matters as much as company and geographic diversification. |

| Not financial advice This page explains the principle of diversification as an educational overview. The examples and portfolio suggestions are illustrative, not tailored to your personal situation. Your ideal asset allocation depends on your age, goals, time horizon, and risk tolerance. Please consider your own circumstances before making investment decisions. |

What Next?

With company, geographic, sector, and asset class diversification understood, the next concept in the Fundamentals section is understanding risk, what investment risk actually is, how to think about your own tolerance for it, and how risk and return are genuinely linked.