Understanding Investment Risk

Risk is the word that stops more people from investing than any other. It sounds like a warning, and in one sense it is. But investment risk is a specific, definable thing that most people misunderstand. Once you understand it properly, it stops being something to fear and starts being something to manage.

This page unpacks what investment risk actually means, the different types that matter, and how to calibrate the right level of risk for your own situation.

What Risk Actually Means in Investing

In everyday language, risk means the possibility of something going wrong. In investing, risk has a more precise meaning: it’s the degree to which the value of your investment can fluctuate, both up and down, over time.

This is sometimes called volatility. A high-risk investment is one whose value can swing dramatically in short periods. A low-risk investment is one whose value is relatively stable but typically grows slowly. The crucial insight is that risk and return are directly linked, the potential for higher returns almost always comes with higher short-term volatility.

| Risk and return, the trade-off A savings account offers a near-certain return of 3-4% with essentially no risk of losing your original deposit (up to FSCS limits). Very low risk, modest return. A global equity index fund has historically returned 7-10% per year over long periods, but in any given year it might rise 25% or fall 30%. Higher long-term return, but real short-term uncertainty. You cannot get higher expected returns without accepting higher short-term uncertainty. Anyone offering both guaranteed high returns and low risk is either mistaken or dishonest. |

The Different Types of Investment Risk

When investors talk about risk, they’re often conflating several different things. Understanding the distinctions helps you manage each one appropriately.

Market risk

Also called systematic risk, this is the risk that the entire market falls, not just one company or sector, but everything. Market crashes, recessions, and global crises cause market risk. It cannot be diversified away because it affects all investments simultaneously. The way to manage market risk is through time, staying invested long enough for the market to recover.

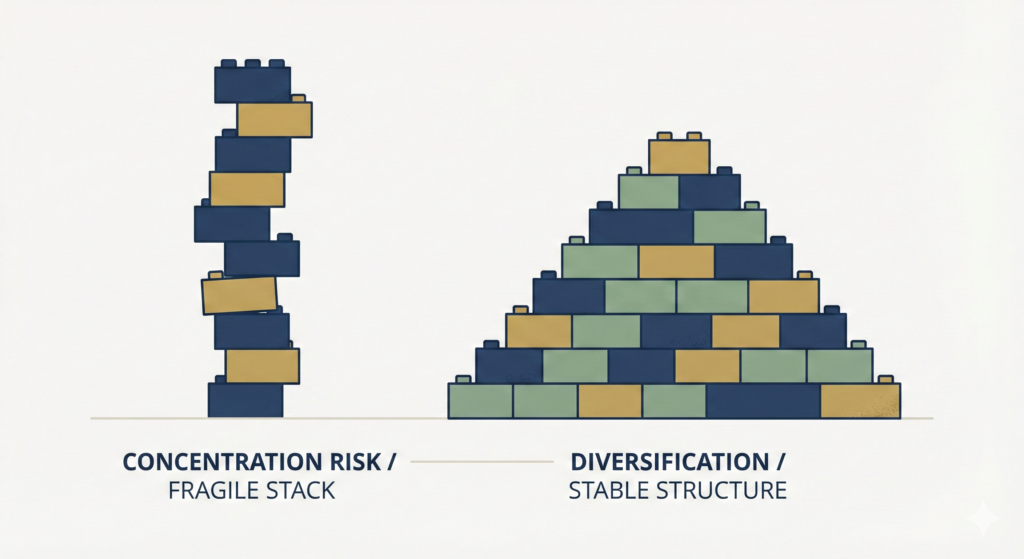

Concentration risk

The risk of having too much money in a single company, sector, or country. If that one thing fails, the damage is severe. This is the risk that diversification directly addresses. A global index fund essentially eliminates concentration risk.

Inflation risk

The risk that your investments don’t grow fast enough to outpace inflation, meaning your purchasing power falls even if your nominal balance rises. Cash is highly exposed to inflation risk over long periods. Equities have historically provided strong protection against inflation because companies can raise prices alongside costs.

Liquidity risk

The risk of not being able to access your money when you need it. Most stocks and ETFs are highly liquid, you can sell them quickly. Some investments (property, certain funds) are much harder to exit quickly. This is why maintaining a separate cash emergency fund is important, you should never be in a position where you have to sell investments at short notice.

Timing risk

The risk of investing at the wrong time, putting a large sum in just before a major market fall. This is the risk that puts many people off lump-sum investing. Regular monthly contributions (pound-cost averaging) spread this risk across many entry points and largely eliminate it as a practical concern.

Behavioural risk

Perhaps the most underappreciated risk of all. The biggest threat to most investors’ returns is their own behaviour, selling when markets fall, chasing recent winners, checking portfolios obsessively, and making emotionally driven decisions. Research consistently shows that the average investor significantly underperforms the funds they invest in, because they buy high and sell low.

| Risk Type | How to Manage It |

| Market risk | Cannot be eliminated. Managed through long time horizons and staying invested. |

| Concentration risk | Eliminated through diversification, global index fund covers this automatically. |

| Inflation risk | Managed by ensuring a meaningful portion of long-term savings is in equities. |

| Liquidity risk | Managed by maintaining a separate cash emergency fund outside investments. |

| Timing risk | Largely eliminated by investing regularly (pound-cost averaging) rather than lump sums. |

| Behavioural risk | Managed by automating investments, not checking portfolios daily, and preparing mentally for volatility. |

How to Think About Your Own Risk Tolerance

Risk tolerance is personal. It depends on your financial situation, your time horizon, and your psychological make-up. Getting this calibration right matters, not because wrong answers lose money, but because taking on more risk than you can emotionally handle leads to bad decisions at exactly the wrong moments.

Two questions help clarify the right level of risk for you:

What is your time horizon?

Time is the most important factor in determining appropriate risk. If you need the money in two years, you cannot afford to have it in equities, a 30% market fall with no time to recover would be genuinely damaging. If you won’t need the money for 25 years, short-term market falls are irrelevant, what matters is the long-term direction, which has historically been strongly upward.

As a rough rule: money you’ll need within 3 years should be in cash. Money you won’t need for 10 or more years can be heavily weighted to equities. Money in between sits somewhere on the spectrum.

What can you emotionally handle?

This is different from what you can financially handle, and both matter. Imagine your £50,000 portfolio shows £32,000 on the screen during a market fall. How do you react? If the answer is ‘I’d panic and sell’, then you’re taking on more risk than is right for you, not because you can’t afford the loss on paper, but because you’ll crystallise it by selling.

Be honest with yourself about this. A slightly lower long-term return from a less volatile portfolio is far better than the real returns most people achieve by getting the psychology wrong.

| The stress test question Before investing any amount, ask yourself: if this fell by 40% tomorrow and stayed there for two years, what would I do? If the answer is anything other than ‘keep investing and wait’, you need to either reduce your equity allocation or invest a smaller amount. Volatility that you can’t stomach rationally leads to selling at the worst possible time. |

Risk by Time Horizon: A Practical Framework

| Risk Level | Typical Asset Mix | Potential Annual Range | Best for |

| Low | 80–100% bonds/cash, 0–20% equities | -5% to +8% | Short time horizons, very low risk tolerance |

| Medium-Low | 40–60% bonds, 40–60% equities | -10% to +12% | 5–10 year horizon, cautious investors |

| Medium | 20–40% bonds, 60–80% equities | -15% to +18% | 10–20 year horizon, balanced approach |

| Medium-High | 10–20% bonds, 80–90% equities | -25% to +25% | 20+ year horizon, comfortable with volatility |

| High | 0–10% bonds, 90–100% equities | -40% to +35% | Long horizon, strong stomach for falls |

These ranges are illustrative. Real market returns are more extreme in both directions. The point is that higher equity allocations mean higher potential swings, and that higher volatility is tolerable over long time horizons because time allows recovery.

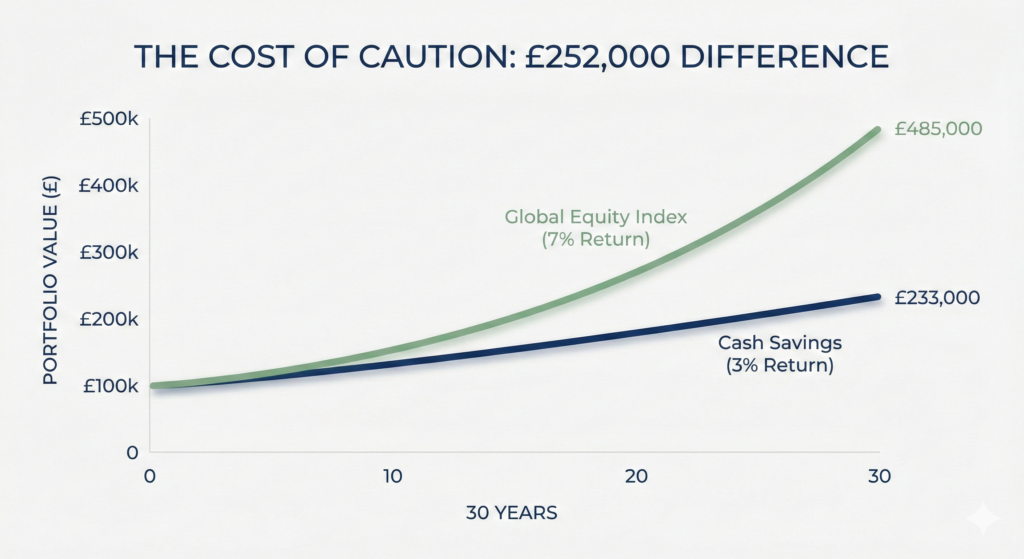

The Risk of Being Too Cautious

Most conversations about investment risk focus on the danger of taking on too much. But for long-term investors, being too cautious carries its own very real risk, the risk of not growing your money fast enough to meet your goals or outpace inflation.

| The cautious investor’s real cost Two investors each save £400 per month for 30 years. Investor A keeps everything in cash savings earning 3% per year. After 30 years: approximately £233,000. Investor B invests in a global equity index fund averaging 7% per year. After 30 years: approximately £485,000. Investor A’s caution cost them £252,000. The money was always ‘safe’ in a savings account, but the real cost of that safety was enormous over a long time horizon. |

For long-term goals, retirement, financial independence, long-term wealth building, the risk of not investing in equities is often greater than the risk of investing in them. This is a counterintuitive point that takes time to internalise, but the maths is consistent.

Practical Steps to Manage Risk Well

- Match your equity allocation to your time horizon, longer horizon means you can accept more volatility

- Diversify broadly, a global index fund eliminates concentration risk automatically

- Keep an emergency fund in cash, so you never have to sell investments at short notice

- Invest regularly rather than in lump sums, removes timing risk from the equation

- Automate your investments and check your portfolio infrequently, removes behavioural risk

- Prepare mentally for falls before they happen, they are inevitable and temporary

| Not financial advice This page explains investment risk as an educational overview. The frameworks and examples are illustrative. The right level of risk for your portfolio depends on your personal circumstances, goals, and financial situation. If you are unsure, consider speaking to a qualified financial adviser. |

What Next?

With a clear understanding of risk, the final concept in the Fundamentals section is rebalancing, what it is, why portfolios drift over time, and how often you actually need to do it. After that, the UK Investing section gets into the practical specifics of ISAs, pensions, and platform comparisons.