What is Rebalancing?

If you invest in more than one fund, say a global equity fund and a bond fund, the proportion of each in your portfolio will drift over time as the two perform differently. Rebalancing is the process of periodically returning your portfolio to its intended allocation.

It sounds technical, but the concept is straightforward. And for many readers of this site, the honest answer to ‘do I need to do it?’ is: probably less often than you think, and possibly not at all if you’re using a single fund.

Why Portfolios Drift

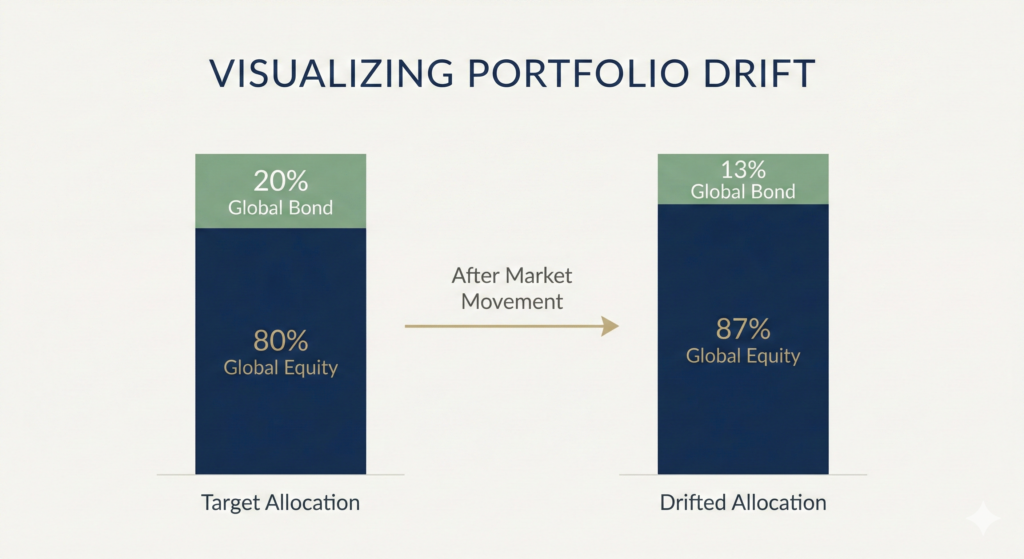

Imagine you start with a simple two-fund portfolio: 80% in a global equity index fund and 20% in a global bond fund. This allocation reflects your intended risk level, you want mostly equities for growth, with a bond cushion for stability.

Over the next five years, global equities have a strong run and your equity fund grows significantly faster than your bond fund. Without you doing anything, your portfolio might now look like 88% equities and 12% bonds. Your risk level has crept higher than you intended, not because you made a decision, but because markets moved.

| Portfolio drift in practice January 2020, Starting portfolio: Global equity fund: £40,000 (80%) Global bond fund: £10,000 (20%) Total: £50,000 January 2025, After strong equity growth: Global equity fund: £68,000 (87%) Global bond fund: £10,200 (13%) Total: £78,200 Your intended 80/20 split has drifted to 87/13 without a single decision being made. You now carry more equity risk than you originally chose. |

Rebalancing corrects this drift, either by selling some of the outperforming asset and buying the underperforming one, or by directing new contributions toward the underweight asset until the balance is restored.

The Two Main Approaches

Sell and buy to rebalance

You sell some of the overweight asset (in our example, some equity fund units) and use the proceeds to buy more of the underweight asset (bond fund units) until you’re back to 80/20. This restores your allocation immediately and precisely.

The potential downside is tax. Inside an ISA or pension, there’s no tax consequence for selling and rebuying. In a general investment account, selling a fund that’s grown significantly may trigger a capital gains tax event, worth factoring in before rebalancing outside a tax wrapper.

Rebalance through new contributions

Rather than selling anything, you simply direct your new monthly contributions toward whichever fund is underweight until the balance is restored. This is slower but avoids any selling, which makes it tax-friendlier in a general investment account and avoids triggering any exit fees.

For most regular investors who are still contributing monthly, this is the simplest and most practical approach.

| Method | When to Use It |

| Sell and buy | Immediate. Precise. May trigger capital gains tax outside an ISA. Best for large portfolios or those no longer contributing. |

| Direct new contributions | Slower but avoids selling. No tax implications. Best for investors still contributing regularly. Takes longer to restore balance. |

A Rebalancing Example

Here’s what a rebalance looks like in practice for the portfolio from our earlier example:

| Asset | Target % | Current % | Action |

| Global Equity Fund | 80% | 87% | Sell excess, reduce by ~£5,500 |

| Global Bond Fund | 20% | 13% | Buy more, increase by ~£5,500 |

After rebalancing, you’re back to your intended 80/20 allocation. Your risk profile matches your original intention. You repeat this process periodically, not constantly.

How Often Should You Rebalance?

This is where many investors overcomplicate things. The research on rebalancing frequency suggests that rebalancing once or twice a year is sufficient for most investors. More frequent rebalancing adds cost and friction without meaningfully improving outcomes.

A practical approach that most investors find manageable:

- Review your portfolio allocation once a year, perhaps in the new tax year in April

- Only rebalance if an asset class has drifted more than 5-10 percentage points from its target

- If you’re contributing regularly, direct contributions toward underweight assets first before selling anything

- Use your annual ISA contribution as a rebalancing opportunity, put new money where it’s needed

| The threshold approach Rather than rebalancing on a fixed schedule, some investors use a threshold, they only rebalance when an asset class drifts more than 5% or 10% from its target. This avoids unnecessary trading in stable markets while still correcting significant drift. For most investors, this means rebalancing rarely, perhaps every few years, which is perfectly fine. |

Do I Need to Rebalance At All?

Here’s the honest answer many sites don’t give: if you’re using a single global equity index fund, you don’t need to rebalance at all. There’s nothing to rebalance. The fund itself is internally diversified across thousands of companies, sectors, and countries. It adjusts its own composition automatically as market caps change.

Rebalancing only becomes relevant when you hold multiple funds with different risk profiles, typically when you add bonds to your portfolio as you get closer to retirement or need to access the money.

| When rebalancing is and isn’t needed Single global equity fund only → No rebalancing needed. The fund manages itself. Equity fund + bond fund → Annual check recommended. Rebalance when drift exceeds 5-10%. Multiple equity funds (e.g. global + emerging markets) → Light-touch annual check. Drift is less dramatic between similar assets. Complex multi-asset portfolio → More regular review appropriate. Consider whether the complexity is necessary. |

The Psychological Benefit of Rebalancing

Beyond the mechanical purpose, rebalancing has a useful psychological function: it forces you to sell what has risen and buy what has fallen. This is the opposite of what human instinct tells us to do.

When equity markets have performed strongly, selling some equities to buy more bonds feels wrong, you’re selling the winner. But doing so locks in some gains, reduces risk, and means you’re buying bonds at a time when they’re relatively cheap. Done over many cycles, this automatic contrarian discipline adds value beyond the pure allocation management.

| Rebalancing as forced discipline “Buy low, sell high” is obvious advice that almost no one follows consistently. Rebalancing builds it into your process automatically. When you top up your underperforming bond fund, you’re buying relatively cheaply. When you trim your overweight equity fund, you’re taking some profit. You’re not making predictions, you’re following a rule. Rules beat instincts in investing. |

Rebalancing Inside a Tax Wrapper

The tax efficiency of your account type affects how freely you can rebalance.

Inside an ISA or pension

You can buy and sell freely without any tax consequence. Rebalancing inside an ISA is completely clean, sell equity fund units, buy bond fund units, done. No capital gains tax, no paperwork, no thresholds to worry about. This is one of the significant practical advantages of keeping your investments inside a tax wrapper.

In a General Investment Account

Selling investments that have grown in value may trigger Capital Gains Tax (CGT) on the gain above your annual CGT allowance (£3,000 in the 2024/25 tax year, significantly reduced from previous years). For investors rebalancing a large general investment account, this is worth planning carefully, the contribution-based rebalancing approach avoids this entirely, and some investors time rebalancing across tax years to use allowances efficiently.

| CGT and rebalancing, get advice if your portfolio is large For general investment accounts with significant gains, the CGT implications of rebalancing can be meaningful. If you’re in this position, it’s worth understanding your annual allowance and potentially spreading rebalancing across tax years. A tax adviser or financial planner can help you do this efficiently. Inside an ISA or pension, this concern disappears entirely. |

A Simple Rebalancing Routine

For the typical investor on this site, using a Stocks and Shares ISA, investing monthly into one or two funds, here’s a practical annual routine:

- Once a year, April is convenient, aligning with the new tax year, check your portfolio allocation

- If you hold a single global equity fund, there’s nothing to do. Move on.

- If you hold equity and bond funds, note the current percentages versus your targets

- If either has drifted more than 5-10%, consider rebalancing

- First option: direct next few months’ contributions toward the underweight fund

- Second option: sell some overweight fund and buy the underweight one (ISA only, to avoid CGT)

- Record the date and allocation, review again next April

| Not financial advice This page explains rebalancing as an educational concept. The examples, thresholds, and approaches described are illustrative rather than prescriptive. Tax rules, including CGT allowances, change annually and may differ from those quoted here. Please verify current rules and consider your own circumstances before making any investment decisions. |

What Next?

The Fundamentals section is now complete. You have everything you need to understand how long-term investing works, why passive index funds make sense, how to manage risk and fees, and how to keep your portfolio on track over time.

The next section is UK Investing, where the principles meet the practicalities. Starting with the Stocks and Shares ISA: what it is, how it works, and why it should be the first account almost every UK investor opens.