Stocks and Shares ISA: The Complete Guide

If you’re going to invest in the UK, the Stocks and Shares ISA should almost certainly be your starting point. It’s the most tax-efficient investing account available to UK residents, it’s simple to open, and the benefits compound beautifully over time.

This guide covers everything, what it is, how it works, the rules you need to know, and how to make the most of it.

| Key Facts at a Glance Annual allowance: £20,000 per tax year (6 April to 5 April) Tax on growth: None, ever Tax on income/dividends: None, ever Tax on withdrawals: None Access to money: Any time, fully flexible Who can open one: UK residents aged 18 or over FSCS protection: Up to £85,000 per provider |

What is a Stocks and Shares ISA?

An ISA (Individual Savings Account) is a government-created account wrapper that shelters your investments from tax. A Stocks and Shares ISA lets you hold investments inside that tax shelter: shares, funds, ETFs, bonds, and more.

The key benefit is straightforward: any growth, income, or dividends your investments produce inside an ISA are completely tax-free, both while the money is invested and when you take it out. There are no thresholds, no annual exemptions to track, and no tax return required. The ISA wrapper handles it all automatically.

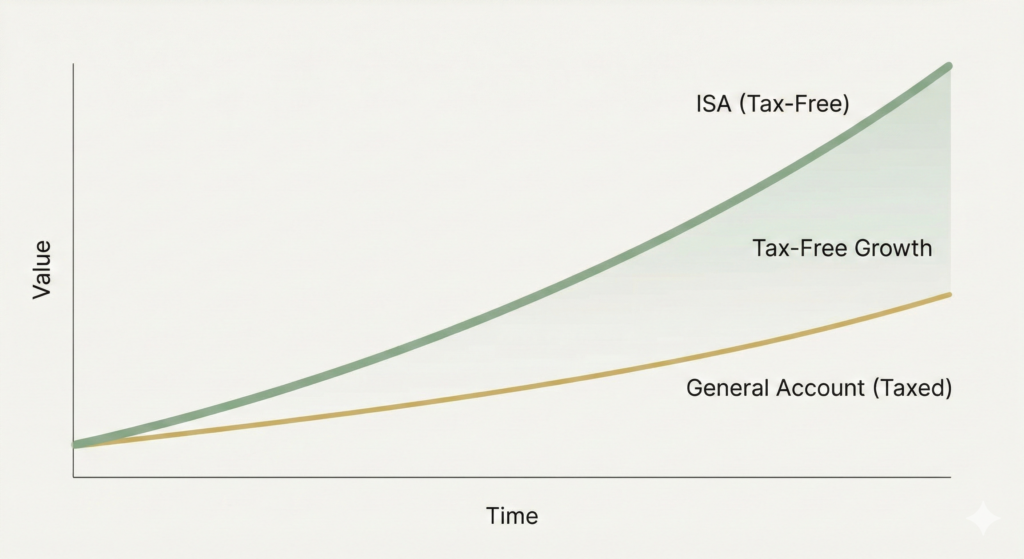

| The ISA advantage in numbers You invest £10,000 in a global index fund inside a Stocks and Shares ISA. Over 20 years it grows to £38,000, a gain of £28,000. Inside the ISA: you pay zero tax on that £28,000. You take out all £38,000, no questions asked. In a general investment account: you’d potentially owe Capital Gains Tax on gains above your annual CGT allowance (£3,000 in 2024/25), and Income Tax on dividends above your dividend allowance (£500 in 2024/25). The exact amount varies by your tax band, but the ISA saves a meaningful sum. The longer you hold investments in an ISA, the more valuable the tax shelter becomes. |

The £20,000 Annual Allowance

Each tax year, running from 6 April to 5 April the following year, you can invest up to £20,000 across your ISAs. This allowance doesn’t carry over. If you don’t use it by 5 April, it’s gone.

Most people don’t come close to the £20,000 limit, and that’s fine, invest what you can afford. But it’s worth being aware of the limit for planning purposes, particularly if you ever receive a windfall, an inheritance, or a bonus that you want to invest tax-efficiently.

| The ISA allowance resets every 5 April A common misconception is that unused ISA allowance rolls over. It doesn’t. Each year you get a fresh £20,000 and last year’s unused portion disappears. If you’re thinking about investing a lump sum, it’s worth checking whether you’re near a tax year end, you may be able to use two years’ worth of allowance by splitting a contribution across 5 and 6 April. |

Flexible vs Non-Flexible ISAs

Some Stocks and Shares ISAs are ‘flexible’, meaning that if you withdraw money, you can replace it in the same tax year without it counting against your allowance again. Most aren’t flexible, and it’s worth checking before you open an account.

| Flexible ISA example You have £20,000 in a flexible ISA and withdraw £5,000 in September. In a flexible ISA, you can pay back in up to £5,000 before 5 April without using any of your annual allowance. In a non-flexible ISA, that £5,000 withdrawal reduces your remaining allowance, you can only pay in £15,000 for the rest of the year. |

What Can You Hold Inside a Stocks and Shares ISA?

The ISA wrapper is flexible in what it can hold, but not everything is eligible. Most mainstream investments are fine:

- Index funds and ETFs, including global equity funds, bond funds, and sector ETFs

- Individual company shares listed on a recognised stock exchange

- Investment trusts

- Corporate and government bonds

- Cash (some providers offer a cash component within the ISA)

You cannot hold physical gold, most alternative investments, or assets not listed on a recognised exchange inside a Stocks and Shares ISA. For most readers of this site investing in index funds, this restriction is irrelevant.

Can I Have Multiple ISAs?

From April 2024, the rules changed, you can now open and contribute to multiple ISAs of the same type in the same tax year. Previously you were limited to one of each type per year.

In practice, most investors are best served by picking one good platform with a Stocks and Shares ISA and sticking with it for simplicity. Splitting your ISA across multiple providers adds complexity for little benefit if you’re investing in similar index funds.

ISA vs General Investment Account: When to Use Each

| Situation | Guidance |

| Always use ISA first | Your ISA allowance is a use-it-or-lose-it tax privilege. Always fill it before investing in a general investment account. |

| If you max your ISA | Once you’ve invested £20,000 in a tax year, a general investment account lets you invest without limit, subject to CGT and income tax on returns. |

| If you need flexibility | ISAs allow withdrawal any time with no tax consequence. Pensions lock your money away until at least 57. For money you might need before retirement, an ISA is usually better. |

| If you’re also using a LISA | The Lifetime ISA (LISA) contributes to your overall £20,000 ISA allowance. If you put £4,000 in a LISA, you have £16,000 of Stocks and Shares ISA allowance remaining. |

How to Open a Stocks and Shares ISA

Opening an ISA takes around 15-20 minutes online. You’ll need:

- Your National Insurance number

- A form of ID (passport or driving licence, most platforms verify digitally)

- Your bank account details for funding

- Choose a platform, see our UK platform comparison for a full breakdown of the main options

- Select ‘Stocks and Shares ISA’ as your account type when prompted

- Complete the application, identity verification is usually instant

- Fund your account via bank transfer or debit card

- Choose your investment, for most beginners, a single global index fund is the right starting point

- Set up a monthly direct debit so contributions happen automatically

Common ISA Mistakes to Avoid

- Opening an ISA but leaving the money in cash, you must actively invest the money, otherwise it just sits earning minimal interest inside the wrapper

- Missing the 5 April deadline, the allowance resets and unused amounts are gone forever

- Paying into two ISAs of the same type at different providers before the April 2024 rule change, check if you’re affected by older rules if splitting across providers

- Withdrawing from a non-flexible ISA and then trying to re-contribute, this uses your allowance a second time

- Choosing a platform based on a welcome bonus rather than long-term fees, the ongoing charge matters far more than a one-time incentive

What Happens to Your ISA if You Die?

Your ISA loses its tax-free status when you die, but there’s a spousal exemption. If you’re married or in a civil partnership, your spouse or civil partner can inherit your ISA and maintain its tax-free status through an Additional Permitted Subscription (APS). This effectively lets them add your ISA value on top of their own annual allowance in the year following your death.

For unmarried partners, children, or other beneficiaries, the ISA proceeds form part of your estate and are subject to normal inheritance rules. The tax-free wrapper doesn’t transfer.

Example

See it in practice: Sarah is a 29 year old teacher in Edinburgh who had never invested before. Read how she worked through the decision to open her firstStocks and Shares ISA, chose an index fund, and set up a monthly habit in the Learning by Example section.

Notes

One thing many ISA investors overlook is that while your ISA forms part of your estate on death, your pension does not pass through your will at all. Making sure your pension nominations are up to date is as important as choosing the right platform. The pension and life insurance beneficiaries guide covers exactly this.

What Next?

If you’re under 40 and saving for a first home or retirement, the Lifetime ISA offers a government bonus on top of your contributions, it’s worth understanding alongside the Stocks and Shares ISA. Or if you’re thinking specifically about retirement investing with tax relief on contributions, our SIPP guide covers how pension investing works.

| Not financial advice This page explains how Stocks and Shares ISAs work based on current HMRC rules. Tax rules can change. The figures quoted are accurate for the 2024/25 tax year, always verify current allowances at gov.uk. This is not personalised financial advice. Your individual circumstances may make different approaches more suitable. |