SIPP and Pension Investing Explained

Pension investing is, for most UK workers, the single most tax-efficient way to save for the long term. The government gives you free money every time you contribute, an immediate return before your investments go anywhere. And yet most people significantly under-use their pension.

This guide covers how pensions work, what a SIPP is and who it’s for, the tax relief you’re entitled to, and how pension investing fits alongside a Stocks and Shares ISA.

| Key Facts at a Glance Tax relief on contributions: 20% basic rate (added automatically), 40%/45% claimable for higher earners Annual allowance: £60,000 or 100% of your earnings, whichever is lower Employer contributions: Many employers match or top up workplace pension contributions Access age: Currently 55, rising to 57 in April 2028 Tax-free lump sum: Up to 25% of your pension pot, up to a maximum of £268,275 Tax on withdrawals: Income tax on the remaining 75% when drawn as income FSCS protection: Varies by provider, most SIPP providers are covered |

How Pension Tax Relief Works

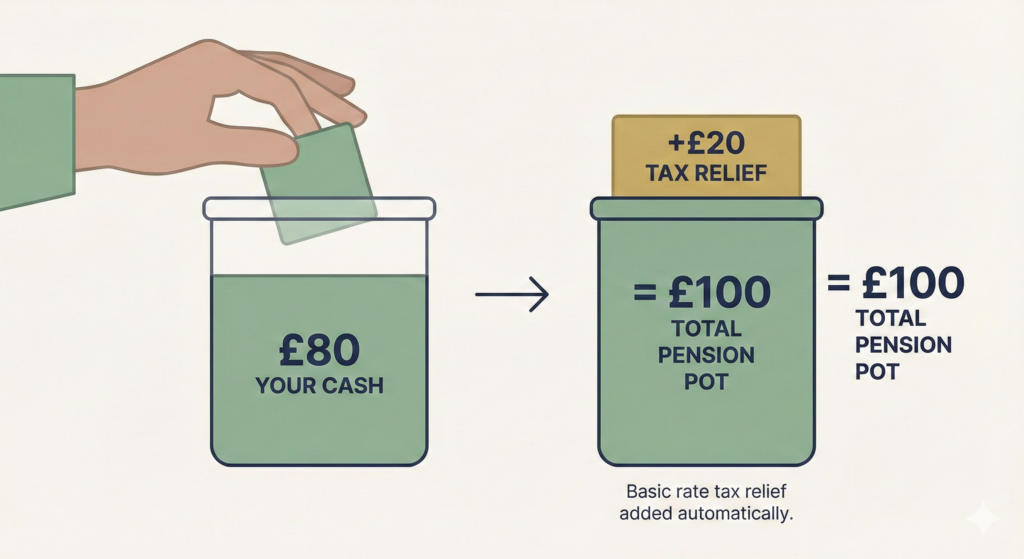

Tax relief is the mechanism that makes pension investing so powerful. When you contribute to a pension, the government tops up your contribution based on your income tax rate. For most workers, this means:

| Tax relief in practice, basic rate taxpayer You want to invest £100 per month into your pension. You only need to pay in £80. The government automatically adds £20, the basic rate tax relief of 20%, making up the full £100. That £20 is money you’d otherwise have paid in income tax. Instead it goes directly into your pension pot. It’s an instant 25% return on your net contribution before your investments grow at all. |

Higher and additional rate taxpayers receive even more generous relief, but the extra relief above basic rate must usually be claimed through a Self Assessment tax return.

| Tax Band | How Relief Works on £100 Contribution |

| Basic rate (20%) | You contribute £80, government adds £20. Full £100 invested. Relief added automatically to most pensions. |

| Higher rate (40%) | You contribute £60, full £100 invested after basic rate relief. Claim extra £20 via Self Assessment. Total relief worth £40. |

| Additional rate (45%) | You contribute £55, full £100 invested after basic rate relief. Claim extra £25 via Self Assessment. Total relief worth £45. |

Workplace Pension vs SIPP

Most employed workers have access to a workplace pension, often a NEST scheme or one arranged through their employer. Self-employed workers and those who want more control over their pension investments often use a Self-Invested Personal Pension (SIPP).

Workplace pension

Your employer deducts contributions from your salary before you see the money, adds their own contribution, and invests it through a pension provider they’ve chosen. The key advantage is the employer contribution, most employers are required to contribute at least 3% of your qualifying earnings, and many contribute more.

Always contribute enough to get your full employer match, this is the single most important pension rule for employed workers. If your employer matches up to 5% and you only contribute 3%, you’re leaving 2% free money on the table.

SIPP (Self-Invested Personal Pension)

A SIPP is a pension you set up and manage yourself, giving you control over where your pension money is invested. You choose the platform, choose the funds, and make the contribution decisions. The same tax relief applies as with a workplace pension, contributions are topped up by HMRC.

SIPPs are particularly useful for:

- Self-employed people who don’t have access to a workplace pension

- Employed workers who want to contribute more than their workplace pension allows, or who want more investment choice

- People who have left employment and want to consolidate old workplace pensions into one place

- Anyone who wants to invest pension money in specific index funds rather than the default funds offered by workplace schemes

The Annual Allowance

You can contribute up to £60,000 per tax year (or 100% of your earnings, whichever is lower) across all your pensions combined, including employer contributions. For most people this limit is irrelevant as a practical constraint. For higher earners it’s worth tracking.

There’s also a carry forward rule, if you haven’t used your full annual allowance in the previous three tax years, you can carry forward the unused portion and contribute more than £60,000 in the current year. This is useful for those who receive a large bonus or windfall they want to shelter in a pension.

| The tapered annual allowance for high earners If your adjusted income exceeds £260,000 per year, your pension annual allowance is gradually reduced, tapering to a minimum of £10,000. If you’re in this bracket, the pension rules become complex and specialist advice is worth having. This affects a very small number of people but the consequences of accidentally exceeding the allowance are significant. |

How to Invest Inside a SIPP

Once you’ve opened a SIPP and funded it, you choose how the money is invested. Most SIPP platforms offer:

- Index funds and ETFs, the same options available in a Stocks and Shares ISA

- Ready-made portfolios, the platform manages asset allocation for you based on your target date or risk level

- Individual shares, for those who want to pick specific companies

For most people investing in a SIPP for retirement, a simple global equity index fund (or a ready-made portfolio that shifts toward bonds as you approach retirement) is entirely adequate. The same principles that apply to ISA investing, low costs, broad diversification, long time horizon, apply equally to pension investing.

ISA vs SIPP: Which to Prioritise?

This is a question most working-age investors face, and the answer depends on your circumstances. Here’s a practical framework:

- First, get your full employer pension match. Always. This is free money.

- Second, consider a Stocks and Shares ISA for any additional saving. The flexibility of ISA access (any time, no penalty) is valuable, especially for goals before retirement.

- Third, if you’re a higher-rate taxpayer, additional pension contributions are very tax-efficient due to 40% relief. Consider topping up your SIPP beyond the minimum.

- Fourth, if you’ve maximised your ISA allowance and want to save more for retirement, a SIPP is the natural next step.

| Factor | Which Wins |

| Access before retirement | ISA, access any time. Pension locked until 57+. |

| Tax relief on contributions | Pension wins, especially for higher-rate taxpayers. |

| Tax on withdrawal | ISA tax-free. Pension: 25% lump sum tax-free, rest taxed as income. |

| Employer match | Pension only, a major advantage for employed workers. |

| Inheritance | Pensions often outside estate for IHT. ISAs form part of estate. |

| Flexibility of use | ISA, use for any goal. Pension, retirement only until 57+. |

Drawing Your Pension

From age 57 (rising from 55 in April 2028), you can start accessing your pension. The options are:

Tax-free cash

You can take up to 25% of your pension pot as a tax-free lump sum, up to a maximum of £268,275. This is a one-time allowance across all your pensions combined.

Flexi-access drawdown

You leave your pension pot invested and draw an income from it as needed. The income is taxed as earned income in the year you take it. This is the most flexible option and allows the remaining pot to continue growing.

Annuity

You exchange your pension pot for a guaranteed income for life, either a fixed amount or one that rises with inflation. Annuity rates improve with age, so this becomes more attractive the older you are when you buy. The income is taxed as earned income.

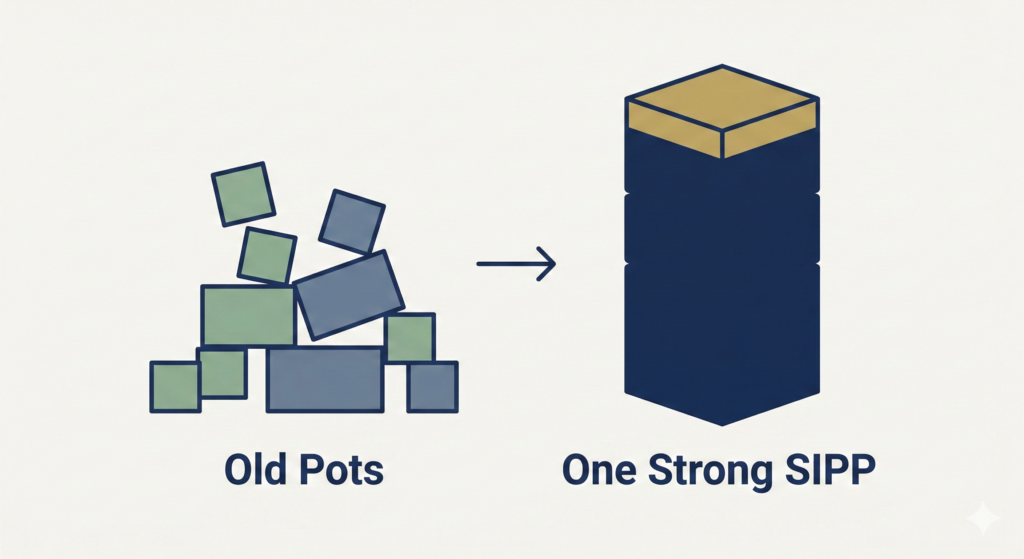

Consolidating Old Pensions

The average UK worker changes jobs numerous times over a career, leaving behind a trail of small workplace pension pots. These are often invested in expensive default funds with no attention paid to them.

Consolidating old pensions into a single SIPP gives you one pot to manage, typically at lower cost and with better investment choice. The process is straightforward, most SIPP providers handle the transfer on your behalf. The key question before transferring is whether your old pension has any guaranteed benefits (such as a defined benefit or final salary element) that would be lost on transfer, these need careful consideration, often with financial advice.

| Finding lost pensions The government’s Pension Tracing Service (gov.uk/find-pension-contact-details) helps you track down old workplace pensions you may have lost track of. It’s free and worth using if you’ve had multiple employers. Even small forgotten pension pots can add up to a meaningful sum when consolidated. |

Example

See it in practice: Marcus is a 34 year old engineer in London who changed jobs and left an old workplace pension behind. Read how he tracked it down, checked for safeguarded benefits, compared charges, and decided what to do with it in the Learning by Example section.

What Next?

With ISA, LISA, and pension investing covered, the next page in the UK Investing section is our platform comparison, a detailed, honest look at the main UK investing platforms for Stocks and Shares ISAs, LISAs, and SIPPs, with the information you need to choose the right one for your situation.

| Not financial advice This page explains pension and SIPP investing as an educational overview based on UK rules current as of the 2024/25 tax year. Pension rules, including access ages, allowances, and tax treatment, are set by HMRC and can change. The decision between ISA and pension contributions depends heavily on your personal tax position, employment status, and goals. Please consider seeking advice from a qualified financial adviser for personalised pension planning. |