Your Savings Rate: The Most Important Number in Your Financial Life

There are many numbers in personal finance that get attention: portfolio size, investment returns, pension pot, house value. But the number that most determines your financial future, more than any of them, is your savings rate.

Your savings rate is the percentage of your income you invest or save each month. It determines how fast you accumulate wealth, how many years you need to work, and ultimately how much financial choice you have in your life. This page explains why it matters so much, how to calculate it honestly, and the most effective levers for improving it.

Why Savings Rate Beats Everything Else

Most people focus their financial energy on investment returns, picking the right fund, timing the market, finding the next great opportunity. But the maths shows that for the accumulation phase of building wealth, savings rate dwarfs investment returns as a driver of outcomes.

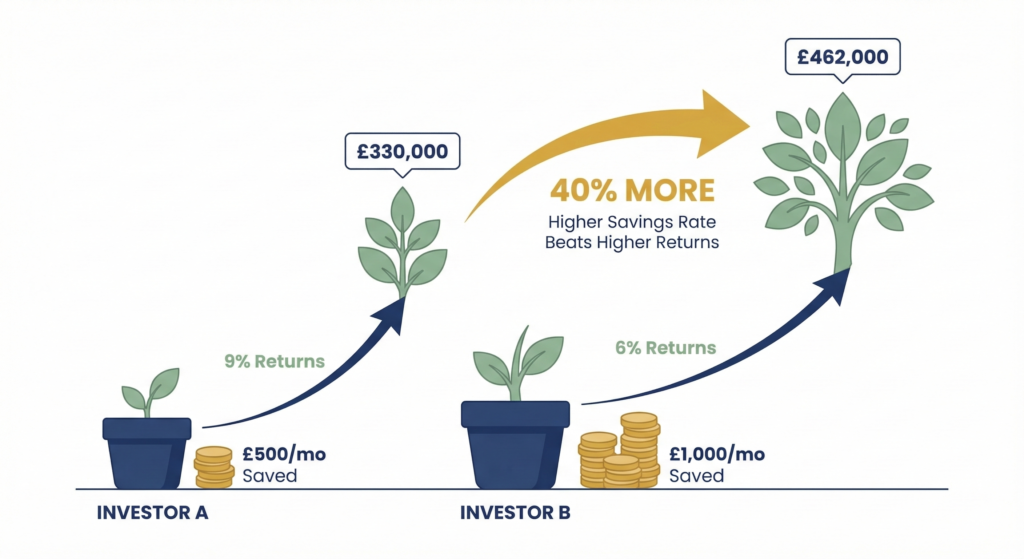

| Savings rate vs returns, which matters more? Investor A saves £500/month and earns 9% average annual returns. Investor B saves £1,000/month and earns 6% average annual returns. After 20 years: Investor A: approximately £330,000 Investor B: approximately £462,000 Investor B ends up with 40% more despite earning meaningfully lower returns, purely because they invested more each month. In the accumulation phase, how much you save consistently beats how cleverly you invest it. |

This changes as your portfolio grows. Once you have several hundred thousand pounds invested, the annual return on that sum starts to exceed your annual contributions, at that point: returns matter more. But for most people in the first 10-15 years of serious investing, savings rate is the primary lever.

How to Calculate Your Savings Rate

There are several ways to calculate savings rate, and different FIRE communities use different conventions. Here’s the most practically useful approach for UK investors:

| Element | How to Treat It |

| What to include as income | Take-home pay after tax and NI. Include employer pension contributions (they’re part of your total compensation going toward savings). Exclude benefits, one-off windfalls. |

| What to count as savings | ISA contributions, pension contributions (yours and employer’s), overpayments on mortgage principal, any other deliberate long-term saving or investing. Do not count cash held in current accounts, only money actively working toward your future. |

| The formula | Savings Rate = (Total Monthly Savings ÷ Total Monthly Income including employer pension) × 100 |

| A useful check | If your savings rate feels surprisingly high or low, recalculate from a different angle: savings rate also equals 1 minus your spending rate. If you spend 60% of your take-home, you’re saving 40%. |

| A worked example Gross salary: £52,000/year → Take-home: £3,350/month Employer pension contribution (5%): £217/month Your pension contribution (5%): £217/month (already deducted from take-home in the above) ISA contribution: £800/month Total income for calculation: £3,350 + £217 = £3,567/month Total savings: £217 (employer pension) + £217 (your pension) + £800 (ISA) = £1,234/month Savings rate: £1,234 ÷ £3,567 = 34.6% Note: the employee pension contribution of £217 is already reflected in the take-home figure, it left before you saw the money. The employer contribution is new money, so it’s added to both sides. |

What Different Savings Rates Mean

| Savings Rate | Approximate FI Timeline | Context |

| Under 10% | ~46 years to FI from zero | Common starting point. Small improvements compound significantly over time. |

| 10–20% | 37–46 years to FI | Better, but a long road. Focus on the biggest spending categories. |

| 20–35% | 23–37 years to FI | Solid. A 30-year career gets you there, working from a normal starting age. |

| 35–50% | 15–23 years to FI | Good progress. FI in mid-career becomes realistic from a typical starting age. |

| 50–65% | 10–17 years to FI | Strong. FI in 40s possible for someone starting in their mid-20s to early 30s. |

| 65%+ | Under 12 years to FI | High performance. Requires either high income, very low spending, or both. |

These figures assume 7% real returns and starting from zero. Your actual timeline will vary, but the pattern is consistent. Every 10 percentage points of savings rate improvement cuts several years off the path to financial independence.

The Six Most Effective Ways to Raise Your Savings Rate

1. Deal with housing costs intentionally

Housing is the largest budget line for most UK households. The difference between spending 25% of take-home on housing versus 40% is enormous, and it compounds over decades. This doesn’t mean choosing misery, it means making the choice deliberately rather than by default, and understanding the FI cost of each housing decision.

2. Stop lifestyle inflation in its tracks

The most powerful savings rate intervention available to most people is simple: when your income rises, save the difference rather than spend it. If you get a 5% pay rise and your spending stays flat, your savings rate jumps significantly. If the pay rise goes straight to a nicer car or a larger flat, it does nothing for your FI timeline.

3. Automate your savings before you can spend them

Set up direct debits for your ISA and pension contributions on payday, the same day your salary arrives. Money that leaves your account immediately is money you don’t miss and don’t spend. Money that sits in your current account finds a way to disappear. Automation removes willpower from the equation entirely.

4. Audit your subscriptions and recurring costs

Most households carry several hundred pounds per month in subscriptions and recurring costs that were signed up for at different times and are never reviewed collectively. A 30-minute annual audit, going through bank statements line by line, reliably finds savings that add up to meaningful monthly improvements in savings rate.

5. Negotiate your salary

Income growth improves savings rate just as effectively as spending cuts, more so if you can hold spending stable while income rises. Salary negotiation is one of the highest-leverage hours most people can spend, yet most never do it. Even a 5% uplift on a £45,000 salary is £2,250/year, several months of ISA contributions added simply by having a conversation.

6. Target your top three spending categories, not everything

Trying to cut every discretionary purchase simultaneously creates resentment and failure. The more effective approach: identify the three largest categories in your spending that don’t directly reflect your genuine priorities, and work on those specifically. High-impact, low-regret cuts do more than a hundred small ones that erode quality of life.

Tracking Your Savings Rate Over Time

A savings rate is most useful as a trend rather than a snapshot. Calculate it monthly or quarterly and track it over a year or more. You’ll see seasonal variation, the impact of pay rises, and the effect of deliberate changes you make to spending or contributions.

The target isn’t a specific number, it’s improvement. Going from 15% to 25% over two years is more meaningful than hitting an arbitrary percentage because the internet said 50% is the goal. Your savings rate should reflect your own priorities and life stage, not someone else’s benchmark.

Your Savings Rate

Enter your monthly take-home pay and expenses to see your current savings rate and what it means for your path to financial independence.

The big number is your savings rate. The bar chart below it shows how your rate compares to common FIRE benchmarks and how many years each rate takes to reach financial independence from zero. The projection chart shows your personal timeline based on your actual numbers.

A few things worth trying:

- Reduce your monthly expenses by £200 and see how much it shortens your timeline

- The difference between a 20% and a 40% savings rate is often less about income and more about housing and transport costs

- Your current savings/investments are included in the projection so the starting point matters too

- The FIRE number updates automatically as your expenses change, lower spending means a smaller target as well as faster progress towards it

| Savings rate and life stage Savings rates naturally vary across life stages. Early career with rent, student loan repayments, and lower income makes high savings rates harder. Mid-career with income growth and stable expenses is typically the highest savings rate window. Having children often reduces the savings rate temporarily. Approaching FI with a paid-off mortgage and higher income is the window for accelerating. Don’t judge your current savings rate against someone at a different life stage. Judge it against last year’s version of yours. |

| Not financial advice This page is an educational overview of savings rate concepts and their relationship to financial independence timelines. The figures are illustrative based on modelling assumptions. Your own financial trajectory depends on many personal factors. Please consider your own circumstances and goals when making decisions about saving and investing. |

What Next?

With a strong savings rate established and money flowing into the right accounts, the next practical challenge for UK early retirement is the ISA-to-pension bridge, structuring your accounts so you can actually access your money between early retirement and pension access age.