Teaching Kids About Money: Where to Start

The most powerful gift you can give a child isn’t a savings account, it’s a healthy relationship with money before they’re old enough to make consequential financial decisions. The habits, attitudes, and basic knowledge formed in childhood and early adolescence tend to stay with people for life.

This section of the site covers everything parents need to know about money and children: age-appropriate lessons, the best savings and investment accounts available for kids in the UK, how to start them investing early, and how to talk about money in ways that build confidence rather than anxiety.

Why This Matters: The Compounding Head Start

The most concrete argument for getting children started with investing early is one any reader of this site will recognise immediately: compound interest.

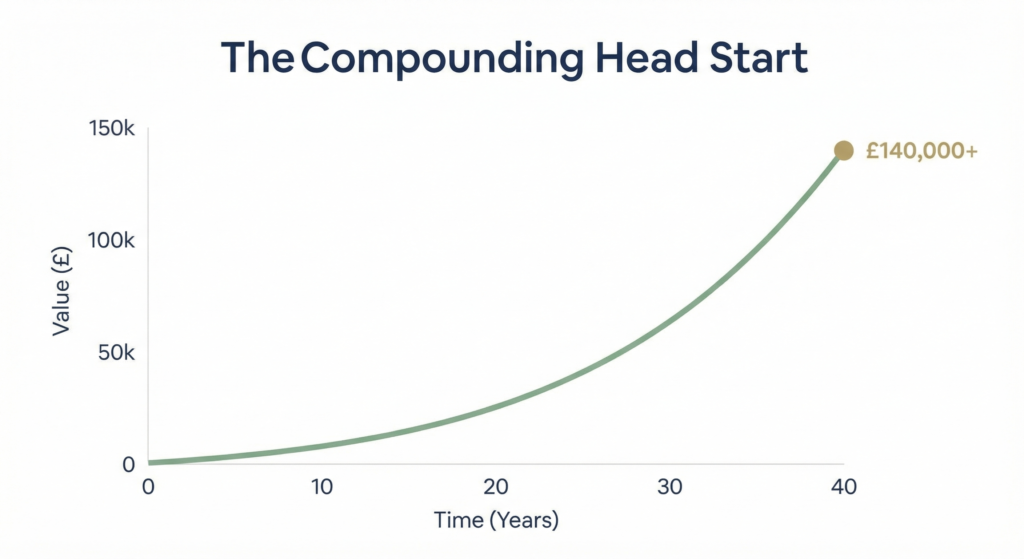

| The gift of time A parent opens a Junior ISA for a child at birth and invests £50/month until the child turns 18. At 7% average annual return, that pot is worth approximately £21,000 at age 18. The child then leaves the money untouched and continues investing £50/month themselves through their 20s. By age 30, the pot is worth approximately £60,000. Alternatively: the child leaves the whole £21,000 untouched from age 18, adds nothing, and lets it compound at 7%. By age 48, that original £21,000 has grown to approximately £140,000, with zero additional contributions. The most valuable investing advantage a child can have is simply starting early. The mathematics are dramatic. |

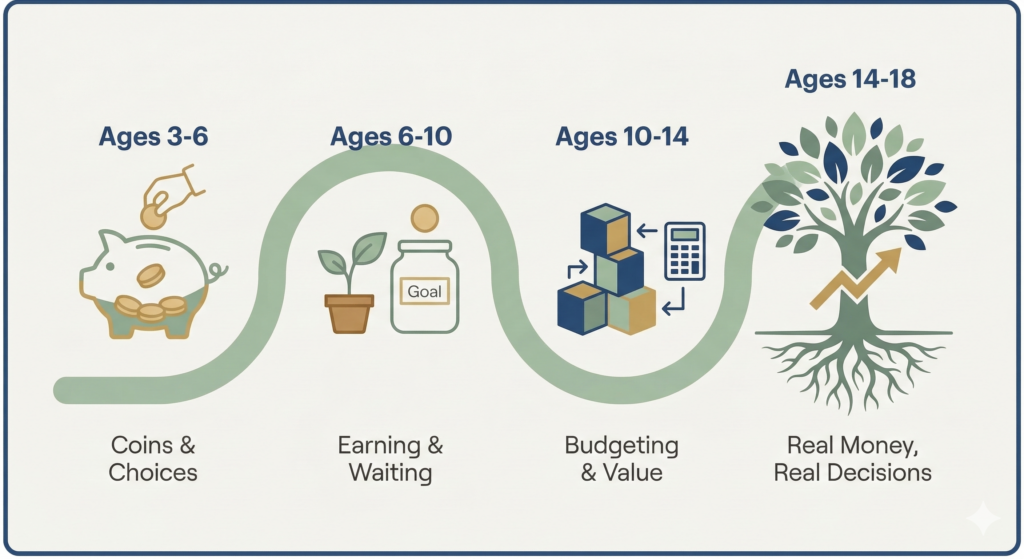

Money Lessons by Age

Ages 3-6: money is real and has limits

The earliest money lessons are physical and concrete. Coins, notes, the concept that you give money to get things, and that when it’s gone it’s gone. A piggy bank with clear sections (spend, save, give) introduces the idea that money can be divided by purpose. The goal at this stage is simply that money is finite and you have to make choices.

Ages 6-10: earning, saving, and waiting

Pocket money, ideally tied to a degree of household contribution rather than given unconditionally, introduces the link between effort and reward. Saving toward something specific teaches delayed gratification, which is arguably the most financially valuable habit that exists. Let them save for something they actually want rather than something you approve of, the lesson needs to be real.

At this age, basic concepts like interest (the bank pays you to leave money with them) and the idea that money can grow can be introduced simply and concretely. Banks like Starling and Monzo offer child-friendly accounts with spending controls that make money management visual and tangible.

Ages 10-14: budgeting and value

Giving a child a fixed amount to manage a broader category of their spending, clothing budget, entertainment budget, builds real budgeting skills. They’ll make mistakes. That’s the point. A mistake at 12 with £30 costs far less than the same lesson learned at 22 with a credit card.

At this stage, introducing the idea of investing, money working for you rather than just sitting, starts to land. The concept of the stock market, what a company is, what owning a share means, can all be explained in plain terms with examples from companies they recognise.

Ages 14-18: real money, real decisions

Teenagers who understand compound interest, basic investing concepts, and the difference between wants and needs are well ahead of most adults. At this stage, showing them the actual numbers, what their Junior ISA is worth, how it’s invested, what it might be worth at 30 or 40 if left to compound, makes abstract concepts concrete and motivating.

Part-time work, managing their own money for larger purchases, and understanding tax basics (what happens to your pay before you receive it) are all age-appropriate lessons that most schools don’t cover.

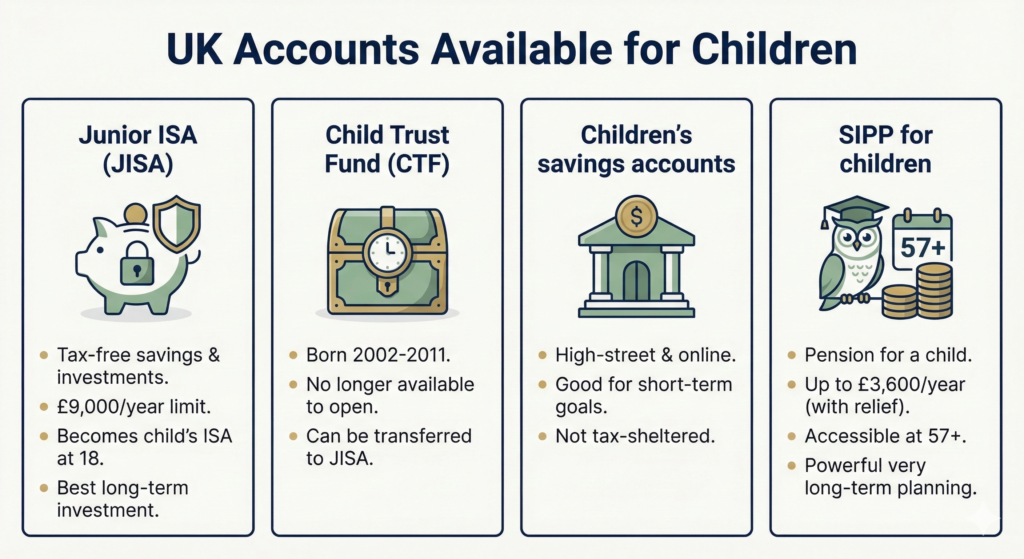

The UK Accounts Available for Children

View full account details and comparisons

| Account Type | What It Is and When to Use It |

|---|---|

| Junior ISA (JISA) | Tax free savings and investments for under 18s. £9,000/year limit. Becomes the child’s own ISA at 18. The best long term investment account available for UK children. |

| Child Trust Fund (CTF) | Government scheme for children born 2002 to 2011. No longer available to open. If your child has one, it can be transferred to a Junior ISA. |

| Children’s savings accounts | High street and online bank accounts for children. Good for short term saving goals. Not tax sheltered for investment growth. Fine for money the child will access in the near term. |

| SIPP for children | You can open a pension for a child, contributing up to £2,880/year (HMRC tops up to £3,600 with basic rate relief). The pension can’t be touched until they’re 57+. Exceptionally powerful for very long term planning but almost invisible as a concept until adulthood. |

What This Section Covers

The Kids & Money section goes deep on each of these areas. The key pages:

- Junior ISA, everything you need to know about opening one, which platform to use, and what to invest in

- Children’s pensions, why they’re so powerful and when they make sense

- Pocket money and financial education, practical approaches by age

- Teaching teenagers about investing, how to make it real and engaging

- When to involve your child in the family’s financial planning

| Not financial advice This page is an educational overview of teaching children about money and the financial accounts available for children in the UK. It is not personalised financial advice. The right approach for your family depends on your own circumstances, goals, and your child’s age and maturity. Please verify current JISA allowances and rules at gov.uk before making decisions. |