Children’s Pensions: The Most Overlooked Investing Tool for UK Kids

Most parents who think about investing for their children consider a Junior ISA. Far fewer consider opening a pension for their child, which is understandable, given that the child won’t be able to access it for 50 or more years. But that inaccessibility is precisely what makes it so powerful.

A pension opened at birth and left completely untouched has the longest possible compounding runway of any financial instrument available. The mathematics are extraordinary, and the tax relief makes it even better.

How a Child’s Pension Works

You can open a Junior Self-Invested Personal Pension (Junior SIPP) for any UK child under 18. The account is managed by a parent or guardian until the child turns 18, at which point it becomes their own pension.

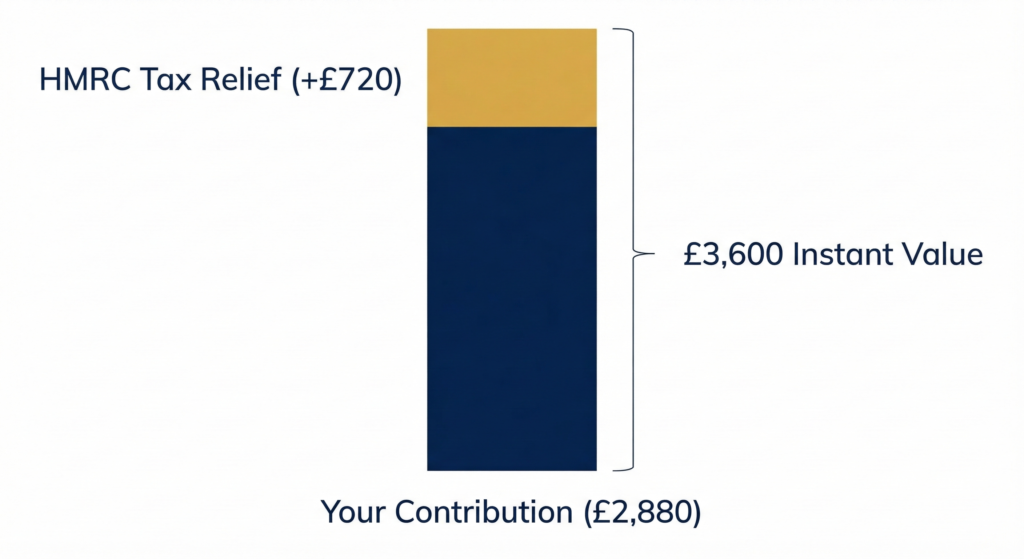

The contribution limit is £2,880 per year in net contributions. HMRC then adds basic-rate tax relief of 20%, topping the contribution up to £3,600. This relief applies even though the child pays no tax, it’s a government subsidy on the contribution regardless of the child’s tax status.

| The tax relief in practice You contribute £2,880 to your child’s SIPP in a tax year. HMRC adds £720 in basic-rate tax relief. The total invested: £3,600. That £720 is free money, you contributed £2,880 and immediately have £3,600 working. The instant return on contribution is 25% before the investments grow at all. Over 18 years of maximum contributions (£2,880/year), the total contributed by the parent is £51,840. With HMRC’s contributions (£720/year), the total invested is £64,800. At 7% average annual returns, this pot is worth approximately £133,000 when the child turns 18, and they can’t touch it until they’re 57+. |

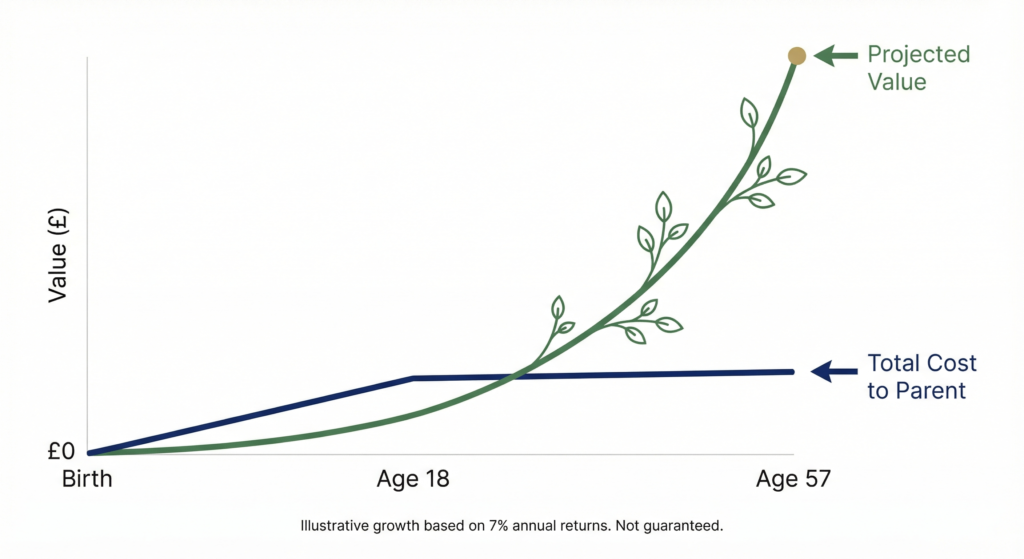

The Compounding Case: Starting at Birth

The real power of a child’s pension is what happens over 50+ years of compounding. The numbers at maturity are difficult to believe until you run them:

On mobile, rotate your screen to see the full comparison

| Monthly Contribution | Parent’s Total Cost | Value at 18 | Projected Value at 57 (no further contributions) |

| £100/month (£1,200/yr) + HMRC top-up | £21,600 contributed over 18yrs | ~£45,000 at 18 | ~£880,000 at 57 (untouched, 7% returns) |

| £240/month (£2,880/yr) + HMRC top-up | £51,840 contributed over 18yrs | ~£133,000 at 18 | ~£2,600,000 at 57 (untouched, 7% returns) |

| £50/month (£600/yr) + HMRC top-up | £10,800 contributed over 18yrs | ~£22,000 at 18 | ~£430,000 at 57 (untouched, 7% returns) |

These projections assume 7% average real returns and no contributions after age 18. They are illustrative, not guaranteed, but they convey the order of magnitude of what compound interest does over 50+ years. A modest monthly contribution started at birth can become a very substantial pension by the time the child reaches retirement age.

| The inaccessibility is the point The biggest objection to children’s pensions is that the money is locked away until 57 (or whatever the pension access age is at the time). This is true, and it’s precisely why it works so well. It cannot be spent on a car at 22, a wedding at 28, or a business idea at 35. It compounds, untouched, for decades. For parents who can afford to set money aside that their child will genuinely not need until retirement, the child’s pension is arguably the single most powerful financial gift available. |

Junior SIPP vs Junior ISA: Which to Prioritise?

Both are excellent. The right split depends on your goals and the amount you can contribute.

| Situation | Approach |

| If the goal is retirement wealth | Junior SIPP, the tax relief and 50+ year compounding horizon makes it exceptional for this purpose. |

| If the goal is a head start at 18 | Junior ISA, accessible at 18, tax-free, convertible to adult ISA. Perfect for university costs, first home deposit, or early career financial foundation. |

| If you can only do one | Junior ISA first, the flexibility of access at 18 is genuinely valuable. The child can open their own SIPP from earned income once they start working. |

| If you can do both | Consider maximum Junior ISA contributions first for the flexible head start, then use any remaining capacity for Junior SIPP for the long-term retirement gift. |

| From grandparents specifically | Junior SIPP contributions from grandparents can have inheritance tax planning advantages, money leaves the estate immediately. Worth discussing with a financial adviser if relevant. |

Practical Considerations

Who can contribute

Anyone can contribute to a child’s Junior SIPP, parents, grandparents, other family members. Total contributions across all contributors cannot exceed £2,880 net (£3,600 gross including HMRC relief) per tax year.

What it invests in

Like an adult SIPP, a Junior SIPP is a self-invested pension, you choose the investments. For a 50+ year time horizon, a global equity index fund is almost always the appropriate choice. Maximum equity exposure, low cost, broad diversification, and 50 years to recover from any downturn.

What happens at 18

The pension becomes the child’s own. They can continue contributing from earned income and benefit from tax relief in their own name. The existing pot continues to compound. They cannot access the money until they reach pension access age (57 from April 2028, verify current rules).

Tax-free cash at retirement

When the child eventually accesses their pension at retirement age, they can take up to 25% as a tax-free lump sum. The remainder is drawn as income, taxed at their income tax rate at the time. A well-structured pot of several hundred thousand pounds, drawn carefully over many years, may attract very little tax.

| Not financial advice This page explains children’s pensions as an educational overview. Pension rules, including contribution limits, tax relief, and access ages, are set by HMRC and change periodically. Always verify current rules at gov.uk. The projections shown are illustrative based on assumed returns and are not predictions of future performance. Please consider seeking advice from a qualified financial adviser, particularly regarding inheritance tax planning aspects. |

What Next?

With investment accounts for children covered, the next page in this section looks at something equally important: the money habits and financial education that make a child capable of using those accounts well when the time comes.